This disclosure applies to Handelsbanken Wealth & Asset Management Limited (HWAM) and Handelsbanken ACD Limited (HACD) in the context of the services provided by HACD or HWAM respectively. Each of HACD and HWAM is authorised and regulated by the Financial Conduct Authority (FCA) in the UK.

Who we are

HACD

HACD is the operator and authorised corporate director of the Handelsbanken Multi Asset Funds (MAFs). HACD has delegated day to day discretionary investment management of the MAFs to HWAM under an Investment Management Agreement. This disclosure sets out the processes that HACD follows where appropriate or requires HWAM to follow in executing and transmitting orders for the MAFs.

HWAM

HWAM offers discretionary services (such as fund and private wealth management), financial planning, custody and execution, and self-select services to its clients.

References to “we” or “us” mean, in the context of the MAFs, HWAM acting as HACD’s delegate investment manager under HACD’s oversight; or in the context of other services provided by HWAM, HWAM. In circumstances where HACD itself is required to execute orders, references to “we” or “us”, in the context of the MAFs only, would mean HACD.

For further information, see below under: Does HWAM treat different types of clients differently?

We are required by the rules of the FCA to ensure that we take all sufficient steps to deliver the “best possible result” for you when executing orders you instruct and when we execute discretionary decisions to trade in assets on your behalf. This is referred to as Best Execution.

We are also required to provide you with a summary of the most important features of our approach to obtaining Best Execution which you can find below. More detailed information about our Order Execution Arrangements is available on request. Please contact us should you wish to obtain more detail.

We are fully committed to ensuring that we clearly define and consistently deliver the best possible outcome for our clients when executing orders on their behalf by following our Order Execution Arrangements and Policy. We continuously assess and monitor the quality of execution against clearly defined execution quality benchmarks.

The very nature of financial markets means it is not always possible for us to guarantee that we will deliver the best possible result for every client order. If we identify an instance where we failed to deliver the best possible result, we will determine whether there were good reasons for not doing so (e.g. dealing in a fast market). If we cannot identify a specific reason, and this becomes a regular or systematic issue, then we will review and update our processes in order to try to deliver the best possible result more consistently.

We are not obligated to proactively disclose to you any failure to achieve the best possible result. However, you do have the right to ask us to demonstrate, on any order we execute on your behalf, how we applied our Order Execution Arrangements and Policy and whether or not the best possible result was achieved for that particular transaction.

We have a number of Retail and Professional clients (as defined by COBS 3 of the FCA Handbook). We offer discretionary services (such as fund and private wealth management), financial planning, custody and execution, and self-select services to our clients. Your specific client categorisation and the type of service you receive is detailed in the Client Agreement or Investment Management Agreement we have with you as relevant.

There are inherent differences between client types, the different services offered and the outcomes agreed for each individual client (e.g. income versus growth). Therefore, rather than taking a “one-size fits all” approach, we approach Best Execution differently for different types of client; by doing so, we are able to focus on the execution factors that are important for each type of client and service offering. Our approach has been developed with regard to best industry practice, regulation and law.

We apply our Order Execution Arrangements and Policy to each client order that we execute. We are required to take all sufficient steps with a view to obtaining the best possible result for our clients, taking into account the following execution factors:

- price;

- transaction costs;

- speed;

- likelihood of execution and settlement;

-size and nature of the order; and

- any other consideration relevant to the execution of an order

When reviewing these execution factors we take into account:

- the characteristics of you as a client, including your categorisation as a Retail or Professional client;

- the characteristics of your order or the portfolio manager's decision to trade on your behalf (as applicable);

- the characteristics of the financial instrument that is the subject of the order; and

- the characteristics of the execution venues to which that order can be directed

We are obliged to deliver the best possible result for clients in relation to all types of financial instruments. However, given the differences in market structures and the structure of financial instruments, it may be difficult to identify and apply a uniform standard of, and procedure for, best execution that would be valid and effective for all classes of instruments. Therefore, we have determined the most important factors for each type of instrument that we may trade on your behalf. We have also defined what we consider to be Best Execution in terms of price. This enables us to take a holistic view of each trade and monitor how well we are applying our Order Execution Arrangements and Policy.

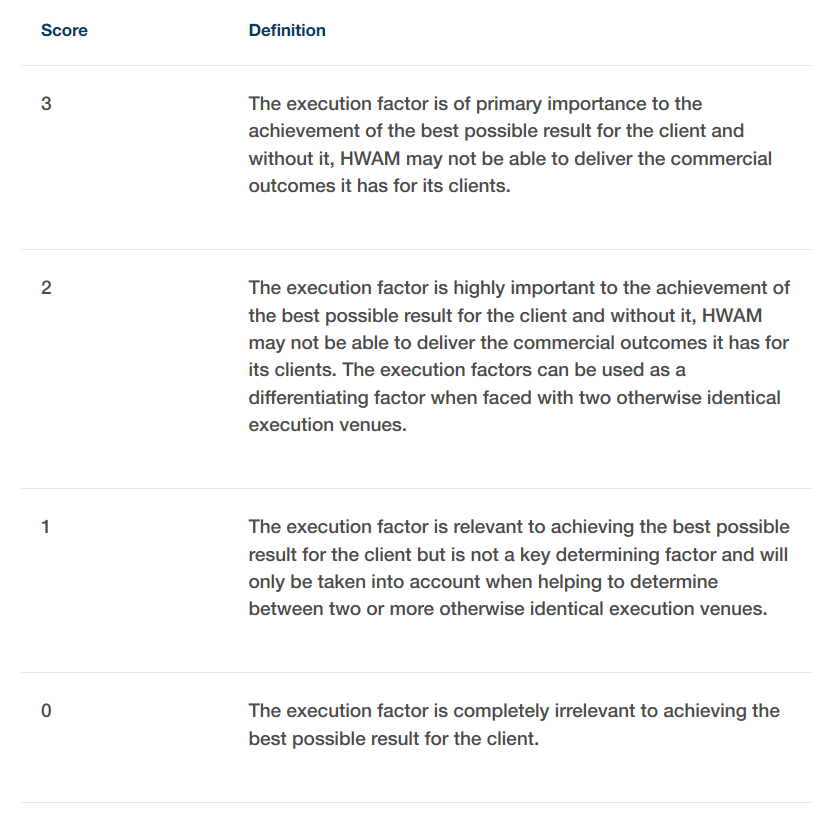

We apply a score to the relevant Best Execution factors (see below) (which also are applied to the choice of execution venue) which are defined below:

In some circumstances, our ability to execute and settle the order will be the primary execution factor. Such circumstances include but are not limited to:

- illiquidity of instruments,

- the size of the order exceeding execution venue settlement limits.

To the extent that it is deemed instrumental to deliver a better overall result for the client and achieve Best Execution, the likelihood of execution and settlement will take precedence over total consideration, representing the price of the financial instrument and the cost related to execution.

The definitions above are subject to review as part of the annual review of the effectiveness of our Order Execution Arrangements and Policy for achieving the best possible results for clients.

The relative importance of the execution factors can be found under sections “Execution Factors According to Client Type, Service Type and Liquidity”, and “The Importance of Execution Factors According to Instrument Type and Liquidity”.

In aiming to deliver the best possible result for you, as a client, we may trade in liquid and/or illiquid instruments. The definition of liquid and illiquid can mean different things according to the type of instrument we are trading and the availability of the instrument to buy and sell at any given time.

In general, we believe that the most important criteria for the execution of orders in liquid instruments are the price of the instrument itself and the costs of the transaction. Other factors may become relevant in specific circumstances which are not envisaged to occur frequently.

The most important criteria for illiquid instruments is the likelihood of execution and settlement. For example, we need to consider whether the proposed transaction will complete in full and in accordance with the terms agreed at the outset of the transaction.

In the case of illiquid instruments, we are required by law to trade in a manner which does not distort the market. In such cases, our primary concern is to ensure we are able to execute the order in a way which does not distort the market and ensure that we are able to settle the transaction so that you obtain the benefits of ownership of that security and its contribution to achieving your investment objectives.

For certain instruments that we may trade, such as convertible bonds, which are not usually traded on an exchange, there may only be one entity making that instrument available to buy or sell in the market. In such cases, it will normally be more important for us to execute the order at the time than to delay the transaction to try and see if other buyers or sellers enter the market and make that instrument available. This is an example of the likelihood of execution and settlement being more important than price and costs.

When executing orders or taking decisions to deal in over-the-counter (OTC) products, including bespoke products, we will check the fairness of the price proposed by gathering market data used in the estimation of the price of the product and, where possible, by comparing the price with similar or comparable products.

The relative importance of the execution factors can be found under sections “Execution Factors According to Client Type, Service Type and Liquidity”, and “The Importance of Execution Factors According to Instrument Type and Liquidity”.

We are required to take all sufficient steps to ensure we obtain the best possible result for you. To enable us to monitor this, we have identified a relevant benchmark for each instrument type and what we consider to be an acceptable level of variance (“slippage”) from that precise benchmark which reflects the margin for error in normal market conditions when we trade for you.

For all of our clients we ensure that:

(a) we carry out the order in accordance with the processes set out in the contract or Terms of Business we have agreed with each client;

(b) we trade in a manner which is not likely to cause price distortions which may disadvantage a client and which might be considered to be market abuse;

(c) we only use an execution venue which has been selected as providing the best possible result for that particular instrument; and

(d) we aim to execute the order at a price within the tolerance of the relevant benchmark and in line with the costs of the chosen execution venue.

The full list of the execution venues that we use in attempting to deliver Best Execution can be found under section “List of Execution Venues”. The list shows which execution venues we use for different instrument types. We regularly review the quality of execution provided by each venue and, therefore, this list may change from time to time without notice.

Please note that we also reserve the right, in very exceptional circumstances, where we are asked or required to trade an unusual instrument not catered for by our existing execution venues, to use an execution venue that is not currently listed. Such events are expected to be rare and “one-off” and we will take sufficient steps to ensure that the execution venue chosen on such a temporary basis is aligned with our requirements in respect of the important execution factors for that type of instrument.

The choice of execution venue will be determined by the execution factors relevant to the type of client and underlying asset classes that we are dealing.

Execution venues include: brokers, regulated markets, multilateral trading facilities (MTFs), organised trading facilities (OTFs), systematic internalisers (SIs), market makers or any other entity which provides liquidity in the market. Subject to any specific instructions that may be given by you, we select those execution venues that we consider to be the most appropriate, taking the execution factors into account (as explained above) as well as qualitative factors such as the credit rating, market access, liquidity, market knowledge, product expertise, order handling process, trading costs, its structure and the systems and controls it has in place.

Under certain circumstances we may select a single execution venue, for example when we participate in a placing or when we are asked to buy or sell a stock that is difficult to trade, such as an illiquid stock. A single execution venue will only be selected where we are able to show that this provides the best possible result for our clients on a consistent basis and where we can reasonably expect that the selected venue will enable us to obtain results that are at least as good as the results that could reasonably be expected from using alternative execution venues.

On an annual basis, we review data published by the execution venues we use concerning the quality of execution they have achieved to ensure that we are obtaining the best result in line with our Order Execution Arrangements and Policy. The most recent data can be viewed and downloaded below.

We may also conduct or commission a broader “Transaction Cost Analysis” (TCA). TCA enables us to determine whether there are execution venues that could achieve better results in terms of costs or price (or both) so that the overall result to you would be an improvement on existing arrangements. Where this is the case, and the costs of switching execution venue are not a barrier, we will change the execution venue so that we can be satisfied we are achieving the best possible result for you.

When transactions are carried out on, and reported to, a regulated exchange (for example the London Stock Exchange) they are considered to be "on-market". Certain transactions (for example most bond transactions) cannot be conducted on-market and where this is the case we will continue to operate on your behalf "off-market". In some circumstances, we may choose to carry out transactions off-market because we believe it is in your best interests to do so. However, there are risks associated with off-market transactions, such as counterparty risk.

In accordance with the FCA rules, we are required to seek your express consent to allow us to execute transactions outside of a regulated market. By entering into your Client Agreement or Investment Management Agreement you have provided this consent. Please contact us at https://wealthandasset.handelsbanken.co.uk/contact-us/ if you have any questions or concerns about this.

We will only act as the execution venue where we believe that it is in your best interests to do so, for example, where we matches a purchase order for one client with a sale from another, rather than going through another execution venue.

Where you provide us with specific instructions – for example, you may specify the size or price of an order or the execution venue on which to trade – while we will aim to apply our Order Execution Arrangements and Policy to your order, we will be bound by your instructions. Delivering on your instructions might prevent us from delivering the best possible result had we not been constrained by your instructions. Please contact us at: https://wealthandasset.handelsbanken.co.uk/contact-us/ if you have any questions or concerns about this.

A limit order is when you instruct us to buy or sell a specific amount or number of shares in an instrument at a specified price or better. When a limit order, which would usually be placed “on-market” or traded on a trading venue, cannot be immediately executed under prevailing market conditions, we are required to make that limit order public unless you instruct us not to. If we are required to make a limit order public, we will be restricted to using only those execution venues who can/will make that limit order public on our behalf and these may not be the execution venues who can give us best execution as described in our Order Execution Arrangements and Policy.

In accordance with the FCA rules, we are required to seek your express consent to allow us not to publicise limit orders. Please contact us at: https://wealthandasset.handelsbanken.co.uk/contact-us/ if you have any questions or concerns about this.

We monitor the effectiveness of our Order Execution Arrangements and Policy on a regular basis and in any event at least annually. Where necessary following these reviews, whenever a material change occurs that affects our ability to continue to obtain the best possible result for you, we will amend our Policy and notify you. Any material changes will be reflected on this page.

A material change would be made as a result of a significant event that could impact the factors affecting execution or the execution criteria stated in our Order Execution Arrangements and Policy.

Execution Factors According To Client Type, Service Type and Liquidity

| Client and Service Type | Liquid - execution factors | Illiquid - execution factors |

Funds | Cost and price – both 3 | Likelihood of execution and settlement – 3, price and costs - 2 |

Private Wealth Management: Retail Clients | Cost and Price – both 3 | Likelihood of execution and settlement – 3, price and costs - 2 |

Private Wealth Management: Professional Clients | Cost and Price – both 3 | Likelihood of execution and settlement – 3, price and costs - 2 |

Custody and Execution: Retail Clients | Price - 3, speed - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Custody and Execution: Professional Clients | Price - 3, speed - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Financial Planning Service: Retail Clients | Speed and price – 3, cost -2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Financial Planning Service: Professional Clients | Speed and price – 3, cost -2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Self-select Clients: Retail Clients | Cost - 3 | N/A |

The Importance of Execution Factors According to Instrument Type and Liquidity

| Instrument | Liquid - execution factors | Illiquid - execution factors |

Equities | Price and costs – both 3 | Likelihood of execution and settlement – 3, price and costs - 2 |

Bonds/fixed income | Price – 3 (costs are in the spread so price paid will be the key determinant) | Likelihood of execution and settlement – 3, price and costs - 2 |

Exchange Traded Funds | Price and costs – both 3 | Likelihood of execution and settlement – 3, price and costs - 2 |

Closed-ended funds | Price and costs – both 3 | Likelihood of execution and settlement – 3, price and costs - 2 |

Regulated open-ended CIS (ICVCs, SICAVs | Likelihood of execution and settlement – 3, price and costs - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Unregulated CIS (UCIS) | Likelihood of execution and settlement – 3, price and costs - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Hedge Funds | Likelihood of execution and settlement – 3, price and costs - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Structured products | Likelihood of execution and settlement – 3, price and costs - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

Foreign exchange | Price (the effective rate less costs) | N/A – very deep and liquid |

FX Forwards (HAF only) | Cost 3, Price 3 | N/A – we will not be dealing in illiquid FX forwards |

Warrants | Likelihood of execution and settlement – 3, price and costs - 2 | Likelihood of execution and settlement – 3, price and costs - 2 |

List of Execution Venues

| Financial instrument | Client type | Execution venue |

Equities (including equity stocks, warrants and depository receipts) | Retail Professional | Bank of New York J P Morgan Securities Ltd Numis Securities Ltd Susquehanna International Securities Winterflood Securities Ltd Jefferies International |

Fixed Income (including gilts and bonds) UK & Overseas | Retail Professional | Bank of New York Citigroup Global Markets Ltd Goldman Sachs Bank Europe SE RBS Global Banking and Markets TRADEWEB Winterflood Securities Ltd |

Open Ended Funds (including Money Market Funds) | Retail Professional | Calastone External Fund Managers Handelsbanken Wealth & Asset Management |

Exchange Traded Funds (ETFs) | Retail Professional | Citigroup Global Markets Ltd Susquehanna International Securities Winterflood Securities Ltd Société Générale, London Branch TRADEWEB Flowtraders Jefferies International Goldman Sachs Jane Street Europe Ltd |

Closed Ended Funds (including Investment Trusts) | Retail Professional | Winterflood Securities Ltd TRADEWEB Bank of New York Numis Securities Ltd JP Morgan Cazenove |

FX | Retail Professional | Bank of New York Northern Trust RBS Global Banking and Markets Handelsbanken UK |

FX Forwards | Per Se Professional | Record Currency Management Limited |

Structured Products | Retail Professional | Citigroup Global Markets Ltd Société Générale, London Branch JP Morgan Cazenove |

Securities Financing Transactions (including repurchases, securities or commodities borrowing or lending, buy-sell back and sell-buy back transactions and collateral swaps) | Professional | We do not currently undertake these types of transactions |