David Absolon Investment Director

20 Feb 2024 8

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

More than half of the world’s population lives in countries holding elections in 2024, including Europe (European Parliament), the UK and the US. Clearly, the US is the most important in terms of impact on the global economy given its leadership of global growth and the potential policies that may result from whoever sits in the Oval Office.

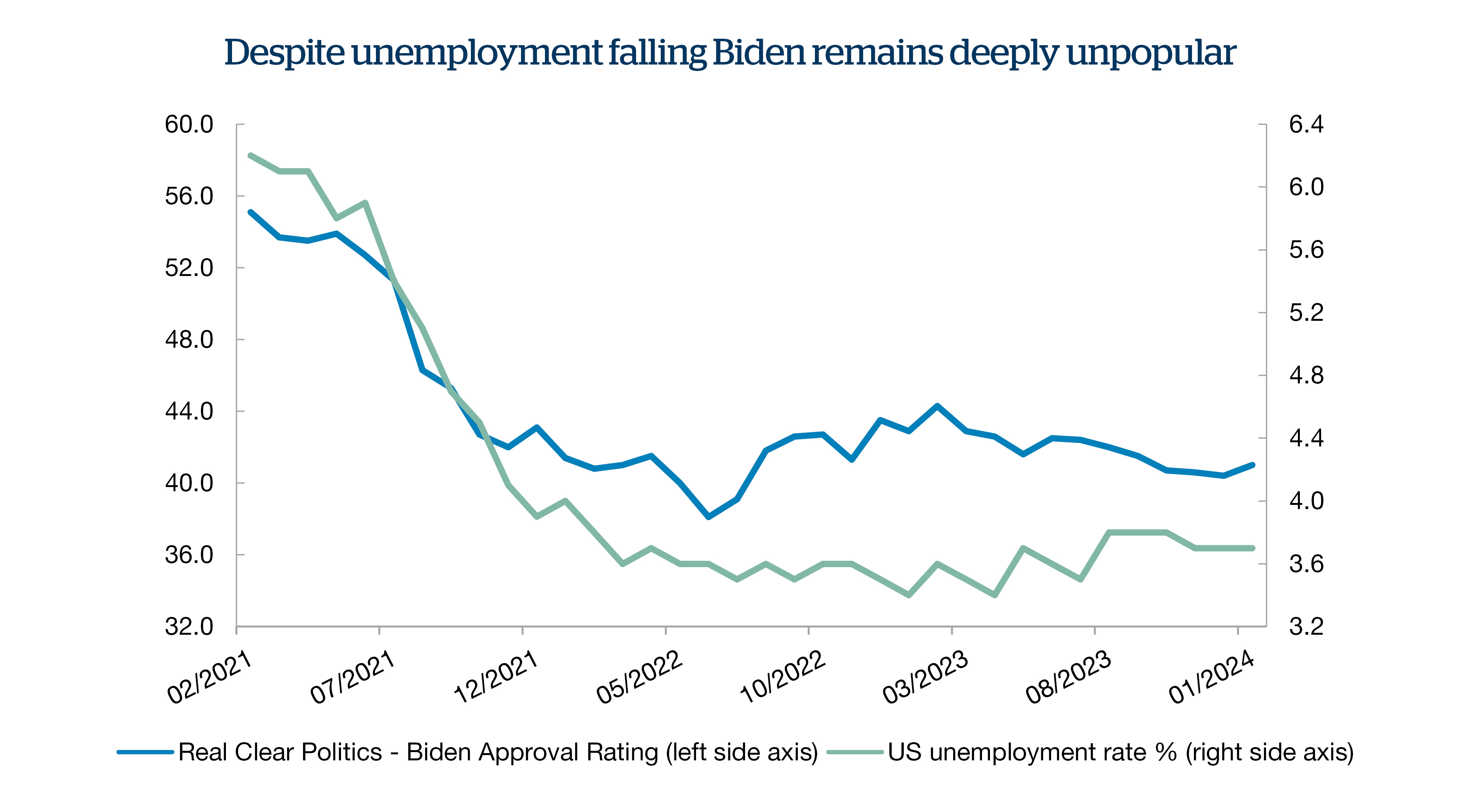

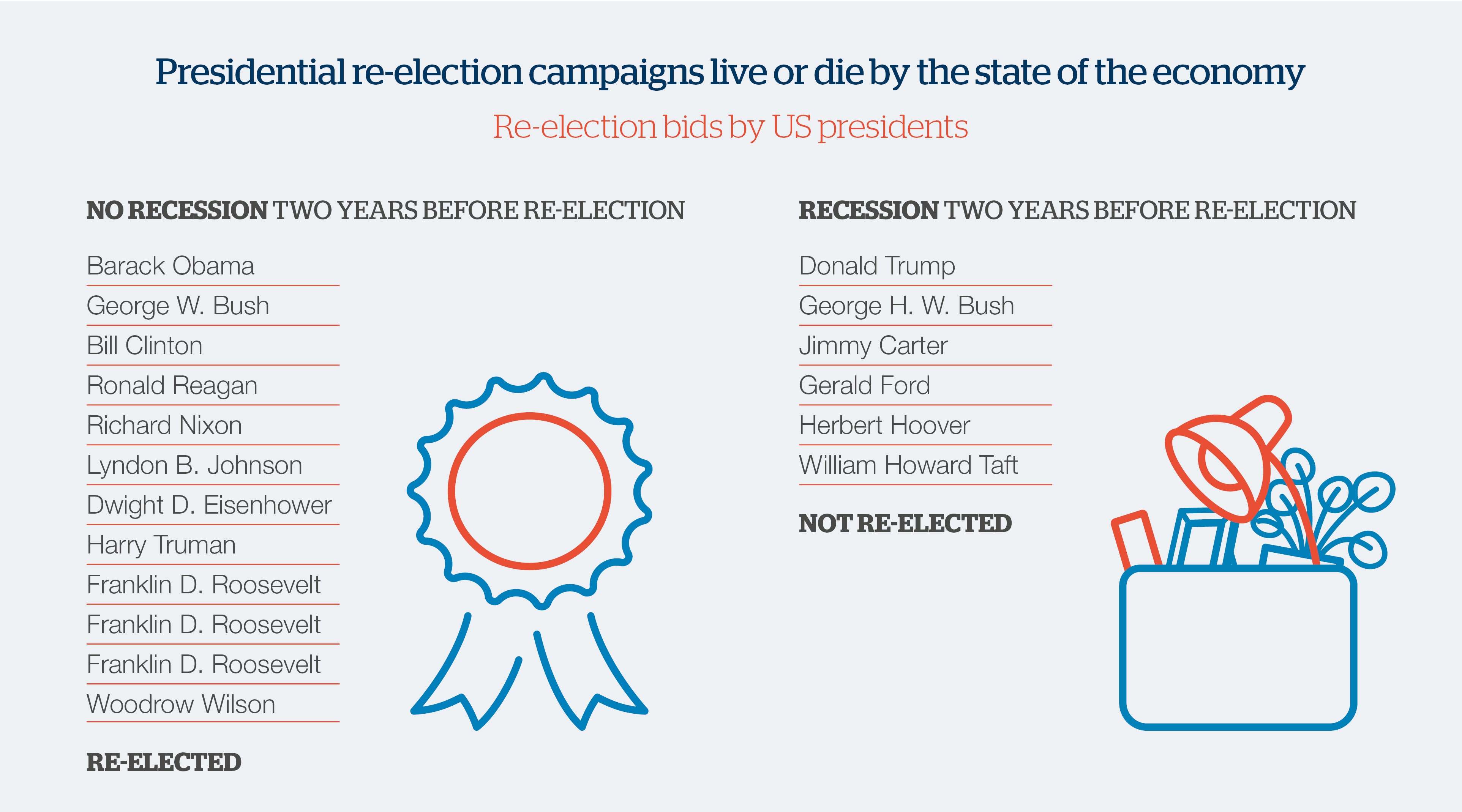

Current indications are that this year’s US election will be a replay of the contest between Presidents Biden and Trump in 2020, although at this point, the outcome remains highly uncertain given Trump’s many legal challenges between now and the election in November. Notwithstanding the current polling, history is on the side of Biden if he can keep the economy out of recession up until then, but he remains hugely unpopular despite a strong US economy and a tight labour market, with questions around his mental competency continuing to dominate the media narrative.

Source: Bloomberg

Source: Strategas

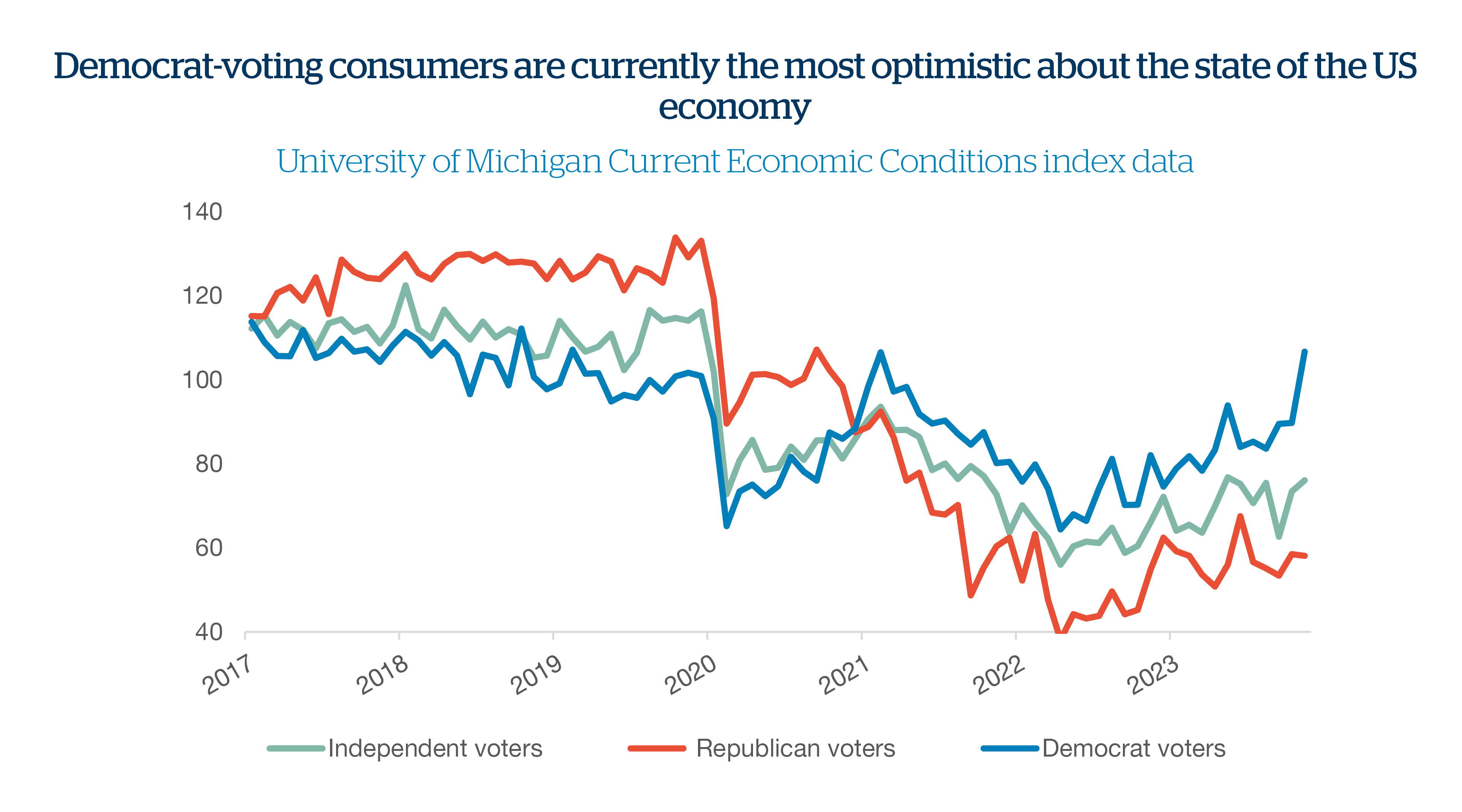

It’s interesting to see that consumer surveys show that while Democrat-voting consumers are optimistic about the economy, both Independent and Republican voters’ confidence around economic conditions is actually below the level it was at the height of the pandemic in 2020. How those Independent voter intentions change between now and November will be key to who ultimately ends up residing in the Oval Office.

Source: Bloomberg

Looking at the polling for the last four elections shows that voting in the US is a 50/50 split. Despite a population of nearly 330 million with around 140 million voting, the states with a ‘tipping point’ vote ultimately decided the election. For Trump to win in 2016 this was 77,744 votes (or 0.06% of the total votes cast) and in 2020 by the same analysis, that number was 65,559 (0.04%) for Biden. Given the way the polls are looking right now, it’s going to be another tight election if the ultimate contest is Biden versus Trump.

This also suggests that whoever does become president, it’s going to be extremely difficult to achieve material majorities in either the Senate or the House of Representatives, making it challenging to pass through any significant changes to fiscal policy. For financial markets this isn’t necessarily bad news as markets prefer certainty around the future path of fiscal policy particularly at times like the present, when significant worries are emerging about the interest cost burden of the very large US deficit. Government prudence, or inactivity, may not be such a bad thing after all in the current climate.

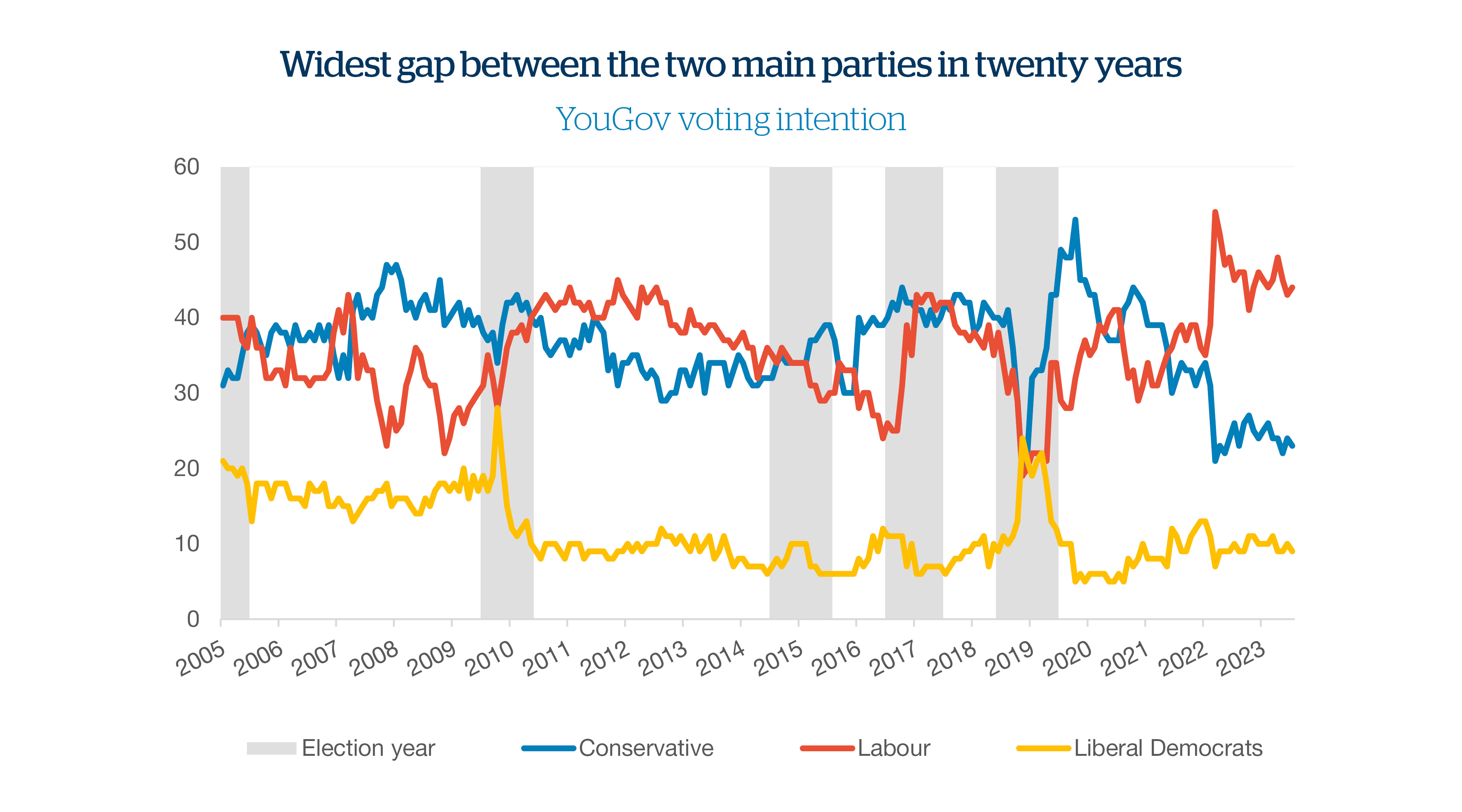

Meanwhile, across the Atlantic it is still too early to make any meaningful assessment of how the UK election will go and at the time of writing, a date has yet to be set. However, current YouGov polling suggests a poor outcome for Prime Minister Sunak.

Compared to this period in the last five elections, Labour are polling higher than they ever have in an election year, albeit the momentum is falling. Aside from 2019, the Conservatives have not polled as low as they are now in an election year based on the last five elections. Boris Johnson did go on to win in 2019, but Labour were also struggling in the polls then as a vote for Labour leader Corbyn at that time was viewed unfavourably. Therefore, public opinion on current Labour leader Keir Starmer would have to deteriorate materially from here for Sunak to achieve a Johnson-type 2019 recovery.

Source: Bloomberg

In 2019, the Electoral Calculus polls correctly predicted both a Johnson victory and its magnitude. With current polling for the 2024 election pointing to a Labour majority, the election is likely to be pushed out well into the second half of the year, giving Sunak a chance to claw back what appears to be an unassailable Labour lead, with ‘sweeteners’ in the spring and autumn budgets.

In the US, if the election outcome was President Biden in the White House plus a Democrat-controlled Congress, we would expect to see an increase in stimulus via another big government spending package. This would likely be good for growth in the subsequent years, and therefore corporate earnings, but bond yields may increase (and bond prices fall).

If the result was Biden in the White House plus a Republican Congress or Trump in the White House with a Democrat Congress, then we see little happening policy-wise over four years and minimal impact on markets.

A combination of Trump in the White House and a Republican Congress increases the chance of fiscal stimulus with an extension of the tax cuts Trump introduced in his previous presidency. This would be good for growth, but Trump could push harder on trade policy, and if history repeats that should be positive for the US dollar.

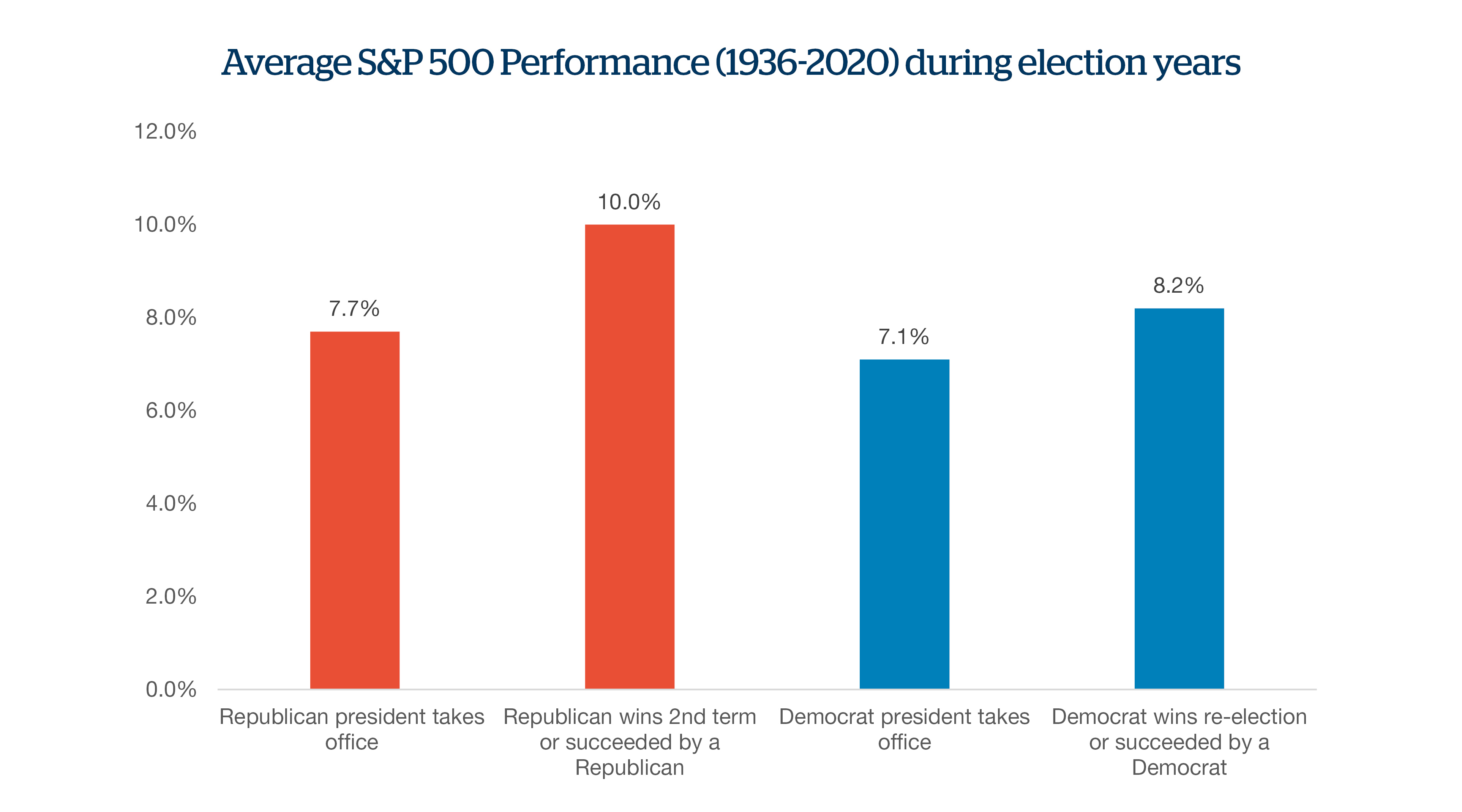

In stock markets, on average the S&P 500 index has produced fertile returns during a presidential re-election year and despite the short-term market volatility that is common within the election season, the historical performance of shares is largely agnostic to which party takes control of the White House.

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

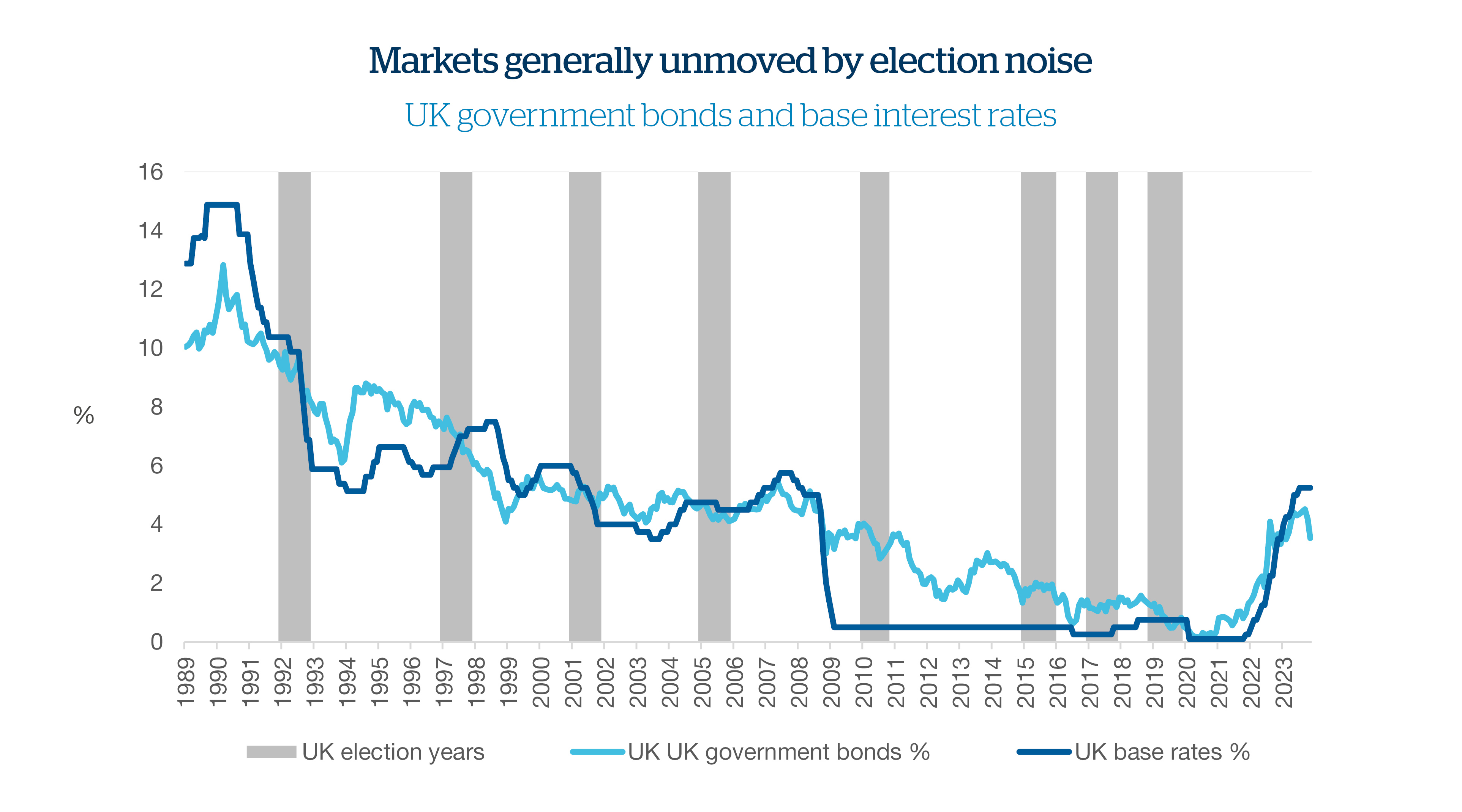

In the UK, if the Labour Party secures a majority under Starmer, whose policies are less left leaning than predecessor Corbyn, we expect little effect on bond yields which will continue to be driven over the long term by interest rate and inflation expectations. Indeed, as the data shows, there is no discernible pattern around bond yields and UK election years. Therefore, our bond views and fixed income asset allocation in our funds will continue to be determined by our view of the macroeconomic backdrop and unfolding monetary policy framework.

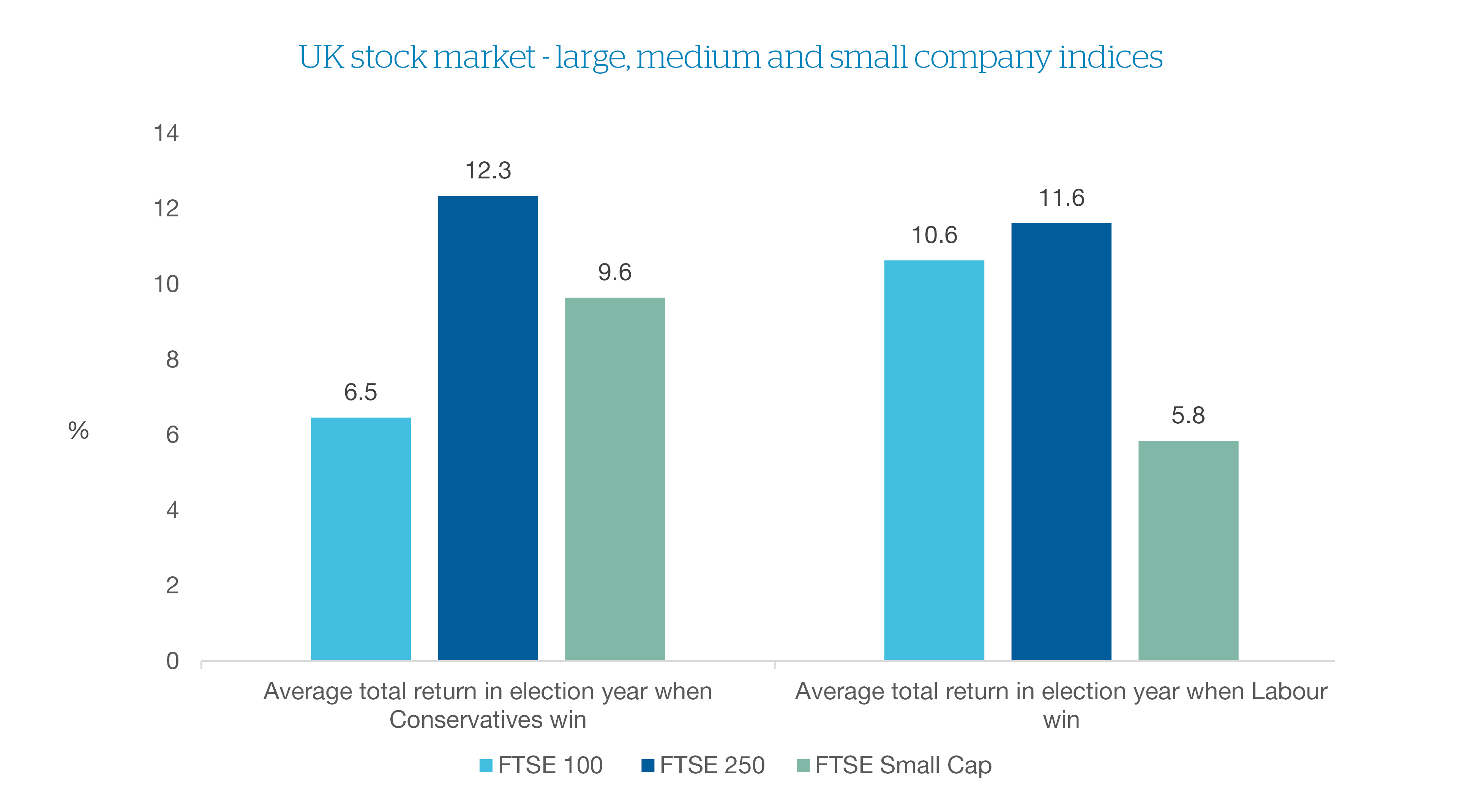

Similar to the US, despite all the noise around elections, on average, election years have provided a fertile environment for UK shares, with positive returns regardless of the government hue. The performance of shares in large and medium-sized UK businesses will be dictated more by global events and the global economy than the UK election, given their global earnings exposure.

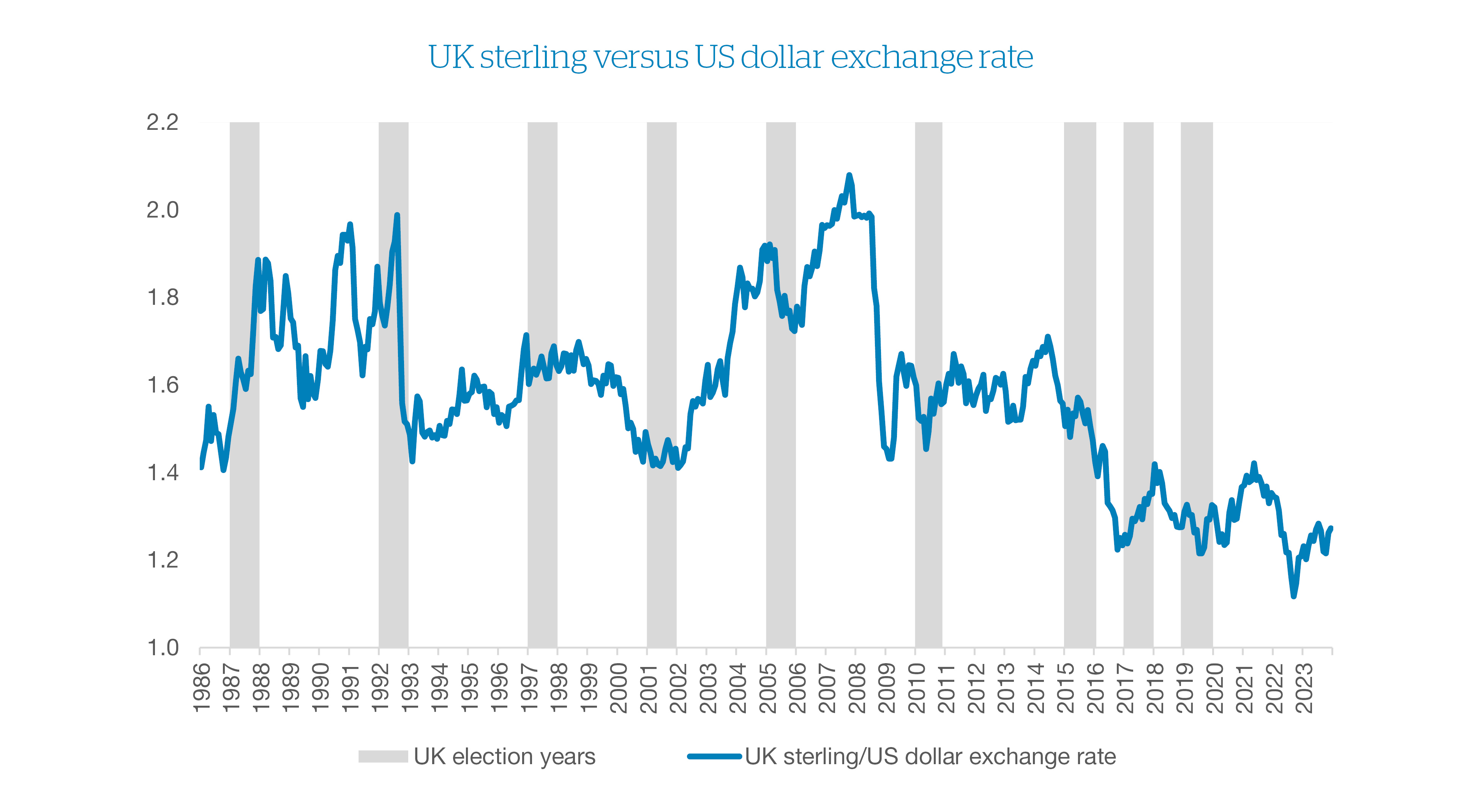

There is also no discernible effect on sterling during election years or from which party wins. The currency is more influenced by prevailing inflation and the interest rate backdrop.

In other words, financial markets largely look through elections and what drives them is the macroeconomic backdrop and monetary policy regime. Our focus therefore remains on long-term investment goals and market fundamentals.