Tax Team Handelsbanken Wealth & Asset Management

17 Feb 2023 12

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

The Chancellor, Jeremy Hunt, presented his Spring Budget to parliament on 15 March 2023.

Whilst the UK’s economic outlook is slightly brighter now than it was last year, public finances remain fragile. Soaring energy bills continue to drive up government borrowing as it funds various packages of support to temper the current ‘cost of living crisis’.

In an effort to expand the UK’s workforce, the Chancellor prioritised pension reform for older workers and support for working parents by expanding the provision of free childcare to children over the age of nine months.

Our Budget note focusses on some of the key tax measures that may be of interest, including many which were previously announced last Autumn.

The Scottish Government maintains control over setting income tax rates and income tax bands over certain types of income. Some of the following income tax measures may therefore not affect Scottish taxpayers.

The income tax personal allowance will remain frozen at its current level of £12,570 until 6 April 2028.

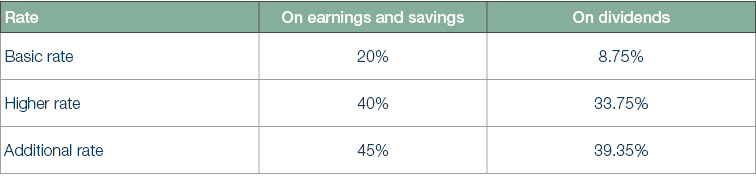

There were no increases to the current headline income tax rates. These remain as follows from 6 April 2023:

The level of taxable income below which individuals will be subject to the 20% basic income tax rate remains at £37,700.

The 40% higher income tax rate applies to taxable income between £37,701 - £125,140.

The threshold above which the 45% additional income tax rate applies will be reduced from £150,000 to £125,140 from 6 April 2023. This reduction will cost most additional rate taxpayers £1,243 extra per year in income tax.

The reduction in the additional rate threshold also means that those with incomes between £125,140 and £150,000 will no longer qualify for the £500 personal savings allowance. This will result in a further income tax liability of up to £225 on savings income.

The reduction of the additional rate threshold to £125,140 now aligns the level at which an individual will be liable to 45% income tax to the level at which their income tax personal allowance is fully abated (by £1 for every £2 of taxable income over £100,000) to zero.

As a result of the withdrawal of the income tax personal allowance, income caught between £100,000 and £125,140 still remains subject to an “unofficial” income tax rate of 60%.

The 0% dividend allowance is set at £1,000 in 2023/24. It is set to halve again to £500 from 6 April 2024.

A basic rate taxpayer may pay up to an extra £87.50 on dividend income from 6 April 2023. The figures for higher rate and additional rate taxpayers are £337.50 and £393.50 respectively.

From 6 April 2024, these liabilities increase still further to £131.25, £506.25 and £590.25.

From 6 November 2022 the previous 1.25% increase to NIC rates designed to fund social care services were reversed.

In 2023/24 employee and employer NIC rates and allowances will be set at their level prior to the abortive 1.25% increase. They will remain at this level until 5 April 2028.

For self-employed individuals, Class 2 NICs will increase by 30 pence and be payable at a rate of £3.45 per week where profits exceed the lower profits threshold.

Class 4 NIC will be payable at a rate of 9% on taxable profits of between £12,570 - £50,270 and 2% on profits above £50,270.

From 2023/24 Class 3 voluntary NIC contributions will increase from £15.85 per week to £17.45.

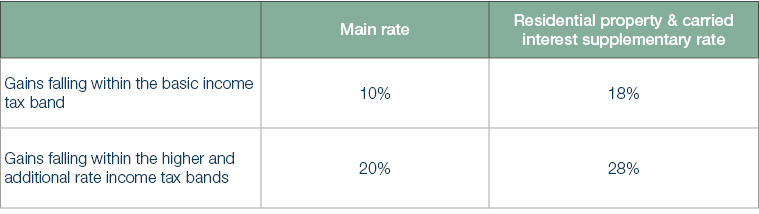

The headline capital gains tax rates remain as follows from 6 April 2023:

From 6 April 2023, the rate of CGT applied remains at 10% and the lifetime allowance at £1 million. An individual must continue to make a “material disposal of business assets” to qualify for BADR.

The 10% CGT rate on qualifying capital gains up to a lifetime limit of £10 million is maintained from 6 April 2023.

The CGT annual exemption will fall significantly from its current level of £12,300 to £6,000 from 6 April 2023.

It will be halved again from £6,000 to £3,000 from 6 April 2024.

The reduction in the CGT annual exemption means that a higher rate taxpayer who would have previously used their full £12,300 exemption could pay up to £1,764 more in CGT in 2023/24 and up to £2,604 more in 2024/25 when compared to 2022/23.

Trustees will also be affected by the change. The CGT annual exemption for trustees is usually set at half of that for individuals.

The CGT annual exemption for trustees will therefore fall to £3,000 in 2023/24 and £1,500 for 2024/25. However, the level of a trustee’s CGT annual exemption will be reduced further where the settlor has established more than one trust.

From 6 April 2023, transfers of chargeable assets between spouses and civil partners who are in the process of separating will be deemed to take place at ‘no gain no loss’ for three tax years following the end of the tax year in which the separation takes place.

Where the transfer is pursuant to a court order, the couple will have an unlimited time to transfer assets and claim no gain no loss CGT treatment.

Furthermore, where a spouse or civil partner retains an interest in the former matrimonial home, they will be given an option to claim Private Residence Relief (PRR) when it is sold.

Individuals who have transferred their interest in the former matrimonial home to their ex-spouse or civil partner, but who are entitled to receive a percentage of the proceeds when the property is eventually sold, will be able to apply main residence relief to those proceeds when received.

A change will be made to self-assessment tax returns for individuals and trustees that will require them to separately identify the disposal of cryptoassets in the capital gains tax pages.

The changes will be introduced in tax returns for the 2024/25 tax year.

From 6 April 2023 the annual investment limit on which individuals may claim income tax relief and CGT reinvestment relief will increase from £100,000 to £200,000.

The age limit that applies to the definition of a company’s ‘new qualifying trade’ at the date of investment will increase from two years to three years. Furthermore, the cap on the level of the company’s gross assets at the time of investment will increase from £200,000 to £350,000.

The ceiling that applies to the investment a company can raise under the SEIS in the relevant period on which investors may claim tax relief increases from £150,000 to £250,000.

The AA is the annual limit on the level of contributions that may be paid into your pension while still benefitting from tax relief.

Where pension contributions (including those paid by an employer) exceed the AA, an income tax charge at your marginal rate will arise on the difference.

Where your adjusted income currently exceeds £240,000 your available AA is gradually tapered down to a maximum of £4,000.

The Chancellor announced that the AA will increase from its current level of £40,000 to £60,000 from 6 April 2023.

Furthermore, the level of ‘adjusted income’ above which tapering of the AA applies will be increased from £240,000 to £260,000. The minimum tapered annual allowance will also increase from £4,000 to £10,000.

For those who are already drawing down on their pension, the total amount they can save each year tax free under the MPAA will also increase from £4,000 to £10,000 from 6 April 2023. Contributions made in excess of where the MPAA applies are taxable at your highest marginal income tax rate.

Most individuals are entitled to take up to 25% of their pension savings as a tax free lump sum called a ‘pension commencement lump sum’ or PCLS.

The maximum that may be accessed in this way will remain frozen at 25% of the current annual allowance resulting in a PCLS limit of £268,275. A higher PCLS may be available to some individuals who have protections in place.

The LTA currently limits how much can be built up in pension savings over your lifetime, while still enjoying full tax benefits, to £1,073,150. It applies to the total of all of your pension savings but excludes any accrued entitlement to the State Pension.

LTA tax charges arise when the aggregate value of pension benefits taken exceeds this limit. The LTA tax charge is currently 55% of the excess where benefits are taken as a lump sum, or 25% where they are taken as income. The tax charges are deducted directly from your pension fund.

Given the UK’s labour shortage, the government came to the view that the LTA acted as a disincentive for individuals, particularly members of the medical profession, to remain in work. A possible increase in the LTA had been widely discussed prior to the Budget but, in a surprise move, the Chancellor announced its outright abolition.

This means that from 6 April 2023 no LTA tax charges will be applied to your pension fund, regardless of the level of pension benefits accrued. The LTA will be formally removed from the statute book from 6 April 2024.

The IHT nil rate band has been fixed at £325,000 since 6 April 2009 and will be maintained at this level until 6 April 2028.

The residential nil rate band, available where an individual leaves their home, or the proceeds from the sale of their home, to a lineal descendent (e.g. children or grandchildren) also remains frozen at £175,000 until the same date.

Given the existing transferablility of unused nil rate bands, estates of a surviving spouse or civil partner can continue to pass on up to £1 million without incurring an inheritance tax liability upon second death.

The rate of IHT applied to estates remains at 40% or 36% where at least 10% of the net estate is left to a registered charity.

The lifetime IHT rate remains at 20% and is payable in certain circumstances such as following the gift of assets to a trust where the value gifted exceeds the settlor’s available nil rate band.

No changes have been made to the existing level of the key IHT exemptions (such as the £3,000 annual exemption and £250 small gifts exemption).

The government will restrict APR and woodlands relief for IHT purposes so that these reliefs only apply to agricultural property and woodlands situated in the UK and not in the EEA, Channel Islands or Isle of Man. The restriction will take effect from 6 April 2024.

The government has also launched a consultation concerning the scope of APR and whether it should be extended to certain types of environmental land management. Consideration will also be given to how long a tenant farmer needs to have farmed the land in order for the owner to qualify for APR.

Following a technical consultation, where a trust or estate receives income of up to £500 per tax year, no income tax will be charged on that income. However, the £500 annual limit will be proportionately reduced to a minimum level of £100 where the settlor has created a number of trusts. The measure will take effect from 6 April 2024.

Following the UK’s departure from the EU, the government will restrict charitable tax reliefs to UK charities and Community Amateur Sports Clubs only. Currently some charities based in the EU or wider EEA benefit from charitable tax reliefs in the UK.

New rules will mean that such overseas charities will only benefit from UK tax reliefs if they are subject to control by the UK courts. The measure will apply from 15 March 2023. Transitional rules will apply to EU and EEA organisations that were previously accepted as charities for UK tax purposes so that they continue to benefit from this status until 31 March 2024.

For UK taxpayers; higher rate and additional rate income tax relief will no longer be available on gift aid donations made to non-qualifying charities in the EU or EEA. It also follows that gifts of chargeable assets to such charities will no longer be exempt from CGT or IHT.

The previously announced increases to the SDLT nil rate threshold in England and Northern Ireland (from £125,000 to £250,000) and the increased nil rate threshold paid by first time buyers (from £300,000 to £420,000) which came into effect on 23 September 2022, will remain in place until 31 March 2025. After this date the thresholds will revert to their previous levels.

Despite some vocal opposition from the government back-benches, the planned increase to the corporation tax rate to 25% for companies with taxable profits over £250,000 will go ahead from 1 April 2023.

The 25% corporation tax rate will also apply to closely held investment companies which will include many family investment companies (FICs).

The 19% smaller companies rate remains in place for those companies where taxable profits are less than £250,000.

Companies within the energy sector will be subject to an Energy Profits Levy of 35% (up from 25% ) until 31 March 2028.

To support business investment and growth, the annual investment allowance will be set at £1 million of qualifying expenditure from 1 April 2023. The level of the allowance is set to be permanent. This means that both incorporated and non-incorporated businesses will be able to write off 100% of the cost of qualifying plant and machinery investments to arrive at their taxable profits each year.

From 1 April 2023 until 31 March 2026 companies will be allowed to write off 100% of their qualifying expenditure on plant and machinery in the year this is incurred.

The full expensing regime is available to companies that are subject to corporation tax. Unincorporated businesses cannot claim it, although they will continue to be able to write off up to £1 million of qualifying expenditure under the Annual Investment Allowance.

For full expensing to apply, ‘qualifying expenditure’ includes certain types of plant and machinery which must be new and unused, must not have been given to the company as a gift or bought to lease to someone else. Cars are specifically excluded from the definition of qualifying expenditure.

Certain types of expenditure may qualify under the ‘special rate’. This does not allow for full expensing but a 50% first year allowance may be claimed instead. Capital allowances may be claimed on the balance at a rate of 6% per annum.

HMRC has launched a new consultation in which it is welcoming views on options to extend the self-employment cash basis. The cash basis offers a simplified way of calculating taxable profits for income tax purposes.

The consultation will focus on various policy proposals including increasing the turnover thresholds to access the cash basis, setting the cash basis as the default option (with an opt-out if the taxpayer wished to adopt the accruals basis) and relaxing restrictions on using relief for losses. The consultation will close on 7 June.

The VAT registration threshold will be maintained at £85,000 and the de-registration threshold at £83,000 until 31 March 2026.

The standard rate and reduced rates of VAT remain unchanged at 20% and 5% respectively.

HMRC has launched a consultation in which it is seeking views about how it could simplify and modernise the administration framework of its ‘income tax services’. The consultation will focus on the PAYE and Income Tax Self Assessment regimes. HMRC is particularly interested in encouraging taxpayers to deal with their income tax affairs digitally to ensure that services are as quick and easy as possible for taxpayers. The consultation will close on 7 June.

HMRC will consult shortly on the introduction of a possible new criminal offence to tackle promoters of tax avoidance schemes who do not comply with legal notices from HMRC to cease their promotion.

The government intends to double the maximum prison sentences for those convicted of the most serious forms of criminal tax fraud from seven to 14 years. However, at this stage it is not known when the measure will come into effect.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340