Investment Team Handelsbanken Wealth & Asset Management

09 Jun 2023 6

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Our investment strategies reflect our views that global growth will slow from here before improving, inflation will remain elevated, and interest rates are close to their peaks.

Bond prices have undergone huge price falls, having been at the centre of 2022’s market storms. We believe these price falls have created an attractive investment opportunity in UK and US government bonds in particular. With this in mind, we have gradually moved from a smaller position in bonds versus our long-term average and a preference for bonds with more limited sensitivity to interest rate changes, to the opposite stance on both fronts. If we’re right about the economic environment ahead, this should help our strategies’ future performance.

Our position in shares, on the other hand, is currently slightly below our long-term average. At the time of writing, we have not been rewarded for this caution in 2023, but we continue to believe that share prices are not adequately reflecting the impact that an economic slowdown is likely to have on corporate earnings. Share prices are better value than they were a year ago, but we’re still not convinced that they represent good enough value to move to a larger position. We have also upped the ‘quality’ of our stock market positions – favouring shares in businesses which should prove more resilient in a slowing growth environment.

Among our ‘alternative’ assets (i.e. beyond traditional bond and stock markets), our gold positions have benefited this year, amid concerns around stubborn inflation and unrest in the banking sector. We continue to dial down (or exit) alternatives positions where the investment rationale was strong in a low interest rate world, but has since waned (our holding in music royalties is a prime example).

This has been an unusual year for stock markets, particularly in the US. Expectations for US interest rate cuts in the second half of 2023 have buoyed the market mood. A further boost has come from the ample liquidity at work in the financial system, as the US Treasury runs down its ‘Treasury General Account’ to counter political fights over government spending limits (the ‘debt ceiling’).

However, we believe these market friends will become foes later in the year for three reasons. First, inflation is likely to remain sufficiently above the central bank’s target, so we do not believe US interest rate cuts are imminent. Second, the Treasury General Account will need to be rebuilt once an agreement is reached on the debt ceiling, reducing liquidity in the financial system. And third, any debt ceiling agreement will involve austerity measures, further risking future economic growth.

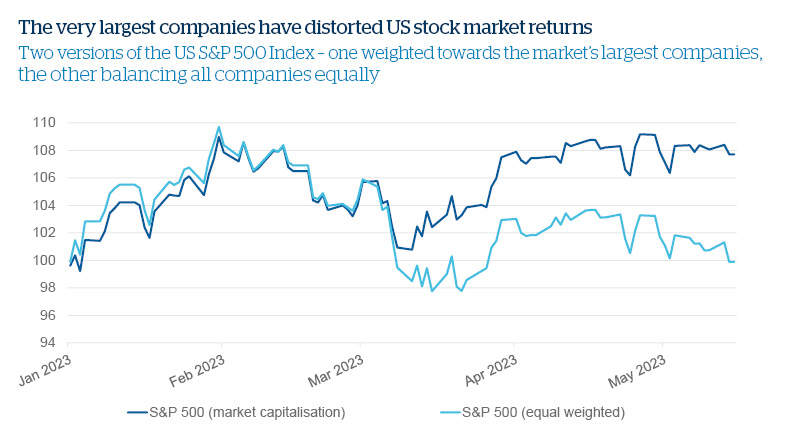

Adding to the distortion, leadership in the US stock market – as measured by the S&P 500 Index – has been very narrow. The S&P 500 is a representative index, made up of shares from the 500 largest US-listed companies. It takes a ‘market capitalisation’ approach, meaning that it assigns more importance (or ‘weight’) to the shares of large, expensive companies. Big movements in the share prices of these companies can therefore significantly impact the S&P 500’s overall value.

So while the S&P 500 Index has risen by nearly 8% so far in 2023 (in US dollar terms), this is almost entirely down to the strong performance of just a handful of very large tech companies. If we look at companies in the S&P 500 on an ‘equal-weighted’ basis (i.e. each company is afforded the same importance, regardless of its size on the market), the S&P 500 would have fallen by almost 1% over the same time period.

Source: Bloomberg

This very narrow stock market leadership has been challenging for our investment strategies. Technology is one of our favoured market themes, but building global and well-diversified strategies is one of our core aims: we would never make our strategies too reliant on a single, concentrated area of the market (where outperformance will not last forever). If anything, despite the short-term pain to our investment strategies, the current narrow focus of stock market returns gives us even higher conviction that our cautious stance remains appropriate.

Source: Factset

It’s impossible to know the ideal time to invest, and we always caution against trying to ‘time the market’ to perfection. As a general rule of thumb, we tend to advise that it’s better to invest when you are able to do so for a period of at least five years, and to look beyond the everyday ups and downs of the market during this time – however hard this may feel in practice.

A buy-and-hold strategy like this is certainly not easy: it requires patience and discipline. There may be prolonged periods when an investment strategy does not appear to be working, but it should ultimately emerge stronger as investments capture positive returns across long-term market fluctuations. We believe that taking a long-term approach and spending time in the market – not timing the market – is what’s important.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340