Investment Team Handelsbanken Wealth & Asset Management

12 Apr 2024 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Inflation is showing clear signs of easing off in most major developed economies. 2022 and 2023’s sharply higher interest rates are playing their part in slowing down economic activity, and taking the heat out of pricing pressures. (As a reminder, lower inflation doesn’t mean that prices are falling, but that the rate at which prices are rising is slowing.)

But while inflation continues to fall, the pace of this has slowed down compared to the more meaningful drops we witnessed in the second half of 2023. Better-than-expected economic survey data has also begun to challenge the view that inflation is headed towards more ‘normal’ levels – close to central banks’ 2% targets – in the near future.

We have long held the view that as the (often very slow) ripple effects of higher interest rates take hold, an economic downturn becomes increasingly unavoidable. Today, the lagged economic effects of higher interest rates are still feeding through into the global economy. In some instances – perhaps most notably the US economy – this has taken longer to show up than we had previously anticipated.

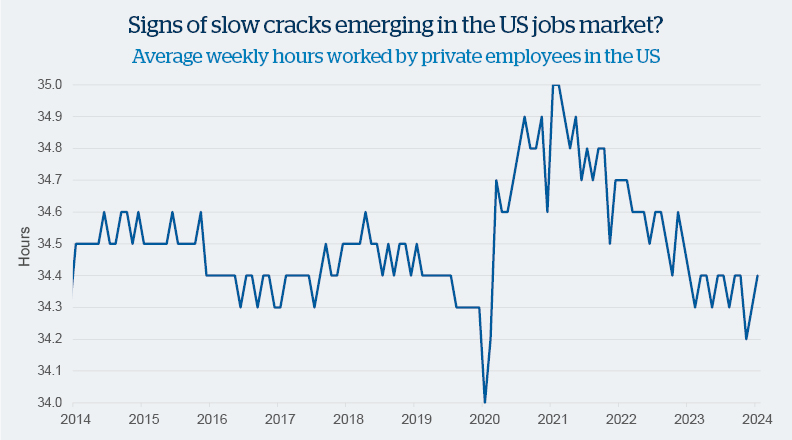

In particular, US employment markets have proven surprisingly resilient in the face of sharp interest rate hikes. However, even here, cracks may be emerging. While employment levels have held up better than expected, hiring is down and the average number of hours worked by employees has also fallen (see our Chart of the Month below). While these might sound like technicalities, we believe that when it comes to economic data, the devil is in the detail.

Pockets of economic resilience around the world mean that the journey towards lower inflation is unlikely to be smooth. Our view has always been that ‘disinflation’ is a process, not a single act. In other words, investors should expect some noise along the way to lower inflation levels.

Investors have been digesting some of this noise in the opening months of 2024, and prices in financial markets suggest that they have broadly adjusted their expectations for the timing and magnitude of future interest rate cuts. Lower interest rates are still expected to arrive this year, but perhaps not so soon, and not so low, as many had previously forecast.

Source: Bloomberg

On the surface, US employment markets look resilient, but the average number of hours worked by employees has generally been reducing since 2021. This means that employers are offering fewer hours of work to their employees. While we may not be seeing mass layoffs, the US workforce is effectively doing (and being paid for) less work than before.

Over the past year, we have reduced our portfolio’s stock market positions in favour of bonds. When we deemphasise a particular asset type within our investment strategies, it doesn’t necessarily mean we feel very negative about that area of the market. Rather, it can mean that we see relatively better options elsewhere. However, this stance does reflect our belief that stock markets would struggle as recessionary pressures build in the global economy.

Within our stock market positions, we hold broad positions giving us broad exposure to major markets, such as a position which tracks the S&P 500 Index. We also hold positions which represent a number of our high conviction ‘themes’: healthcare, technology and insurance.

At the time of this update, we are slightly 'underweight' stock market investments. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in shares versus our long-term average.

In keeping with our predictions of a slowdown in economic growth, our multi asset investment strategies currently hold a higher proportion of assets in fixed income markets (like government bonds) versus our long-term average positions. Having been a rather uninteresting part of financial markets for quite some time, bonds rose higher in 2023 than they had done for many years, presenting what we perceived to be an attractive buying opportunity.

History is never the most reliable guide to future performance, but broadly speaking, as the economic backdrop worsens, bond yields should fall and bond prices (which always move in the opposite direction to yields) should rise. In turn, this should benefit our bond holdings.

Within our multi asset strategies, we have been incrementally building up our bond exposure. This has meant not only increasing the proportion of bonds that our strategies hold, but also the maturity of these bonds, particularly UK government bonds. Adding longer-maturity bonds gives us a greater sensitivity to movements in expectations for interest rates, and we continue to believe the market is underappreciating how much the Bank of England in particular will cut interest rates over the next 12-18 months.

At the time of this update, we are slightly 'overweight' bond market investments. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in bond versus our long-term average.

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds.

Because of their huge variety, it’s difficult to make sweeping statements about alternative assets. We are roughly ‘neutral’ about alternative assets overall, but would note that this headline neutrality hides some specific preferences. At present, we have a preference for assets which can drive financial returns, without being closely linked to mainstream financial markets. Current notable holdings include a specialist hedge fund designed to protect against dramatic market falls.

At the time of this update, we are 'neutral' when it comes to alternative assets. This means that we have not deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in alternative assets which is consistent with our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.