Investment Team Handelsbanken Wealth & Asset Management

14 Aug 2024 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

A noisy patch for financial markets…

Up until the second week in August, markets had become fairly comfortable with the narrative that the US economy was growing, but slowing. However, this started to shift as US economic data began to infer a potentially greater economic slowdown than originally envisaged. This raised questions around the future earnings trajectory of highly-rated US companies.

Against this backdrop, investors began to account (within asset prices) for more interest rate cuts from the world’s largest central bank (the US Federal Reserve, or Fed). As a result, bond yields fell, and bond prices rose.

Around the same time, the Bank of Japan raised interest rates for only the second time since 2007. Although this was well flagged in advance, investors started to predict more rate cuts. This led to concerns about how this would affect the Japanese economy. Japanese share prices dropped with historic speed, and – globally – the price of traditional safe-haven assets like government bonds and precious metals rose sharply. The situation was further exacerbated by low levels of liquidity (buying and selling in the market) due to the summer holiday season.

Nevertheless, by the end of the week, markets were only marginally lower than where they had begun. More US economic data updates signalled that an imminent and severe US recession was not on the cards, and the price of shares and other risky financial assets rallied, with ‘safe havens’ giving back some earlier gains.

… but expectations for interest rate cuts are still very changeable

Market expectations for interest rate cuts from the US central bank have been reacting to weaker US data. In late July, pricing in bond markets told us that investors were expecting two interest rate cuts from the Fed this year, but during the recent market volatility, this spiked to six rate cuts.

As we write, these expectations have come down a little, to four US interest rate cuts this year. It’s worth noting that the Fed’s ruling committee only has three scheduled meetings remaining in 2024, suggesting that one of these rate cuts would need to be double the usual size.

Within our own investment strategies, our bond market positions have benefitted from this environment of weaker economic data and higher expectations for interest rate cuts, including the Bank of England actually cutting rates in August. This marginally surprised investors, who had thought September would be the meeting to cut rates for the first time since the pandemic.

The US presidential election remains one to watch

Since our July update, President Biden has dropped out of the US presidential race, with his erstwhile running mate – Kamala Harris – stepping into the breach. US politics can certainly create noise in financial markets, but the more important issues for us to consider are the economic implications of whoever next steps into the White House.

The betting odds have changed dramatically since Biden dropped out and it now looks like a much fairer and more even fight between the two nominated candidates for the White House race. Trump prides himself on being pro economic growth, but he may have already played his best cards in his previous stint at the top. We’re a little wary of some of the potential policy impact of a second Trump presidency, given his rhetoric around NATO, Ukraine and European and Chinese trade tariffs.

Meanwhile, we wouldn’t expect Harris’ approach to economic and geopolitical matters to diverge hugely from Biden’s, though we’ll have to wait to discover more about her views as her fledgling campaign takes off.

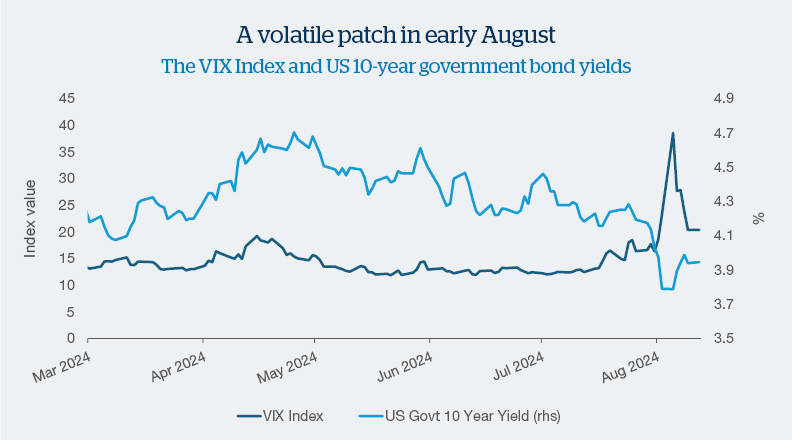

Source: Bloomberg

The dark blue line is the VIX Index (in full: the Chicago Board Option Exchange Volatility Index). This is often referred to as the ‘Fear Gauge’. It’s an up-to-the-minute market estimate of the expected volatility of the S&P 500 Equity Index – the benchmark index for the US stock market.

On the same chart, the light blue line shows us the yield on the US 10-year government bond (as a reminder, bond yields move in the opposite direction to bond prices). You can see how yields fell in early August, as US economic data slowed and the market started to assume a higher probability that the US central bank would not only start to cut rates soon, but also cut rates by more than previously expected. Bond yields fell further as the VIX index spiked in the second week of August, reflecting investor nerves about growth and interest rate changes.

However, since then, the VIX index has retraced much of this spike, suggesting calmer investor sentiment, at least at the time of writing.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are 'neutral' when it comes to stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are slightly 'overweight' bond market investments. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in bonds versus our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340