Investment Team Handelsbanken Wealth & Asset Management

10 Dec 2024 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Economic resilience is encouraging, though we’re mindful of risks

Despite sharply rising interest rates around the world since the COVID-19 crisis, the global economy has remained surprisingly resilient. There are a number of reasons behind this, least not the ongoing boost provided by government economic support packages in response to the pandemic. The combined impact of these measures has been greater than previously anticipated, supporting economic health and consumer confidence for longer.

The US economy has been particularly robust. Looking ahead into 2025, support for this already upbeat (and highly influential) economy is likely to continue. President-elect Trump is expected to keep earlier tax cuts to avoid jolting the all-important US consumers, who have also been enjoying a surprisingly long-run financial buffer through previously built-up savings.

Central banks remain on the lookout for key signals

Generally declining inflation has allowed central banks to begin lowering interest rates in 2024, but there is still much further to go. A critical part of most leading central banks’ mandates includes managing inflation levels in the economy, but they will also be keeping a close eye on other key economic variables – most notably, the labour market.

In the US, demand for labour appears to be abating compared to the available supply of US workers – a somewhat uneasy economic signal. It’s certainly possible that these dynamics develop slowly enough that they are ultimately overtaken by other issues. We’ll be keeping a close eye on the labour market situation, mindful of its potential impact on the outlook for unemployment, consumption and general economic health.

Financial markets have been enjoying this environment

2024 was a much better year for financial returns, from a wide range of asset types, than 2022-2023. Financial markets have welcomed relatively calm economic growth, lower inflation and falling interest rates. While nothing in economics or financial markets is ever static or certain, this feels suspiciously like the ‘soft landing’ that central banks were hoping for.

Our views on the current environment mean that our investment positioning between different types of assets has shifted slightly, as we outline further down the page. We have slightly increased our positions in stock markets, and have slightly reduced our positions in government bond markets. These are relatively small shifts in the balance of assets in our strategies, and we would always expect this balance to be in flux as different opportunities rise and fade.

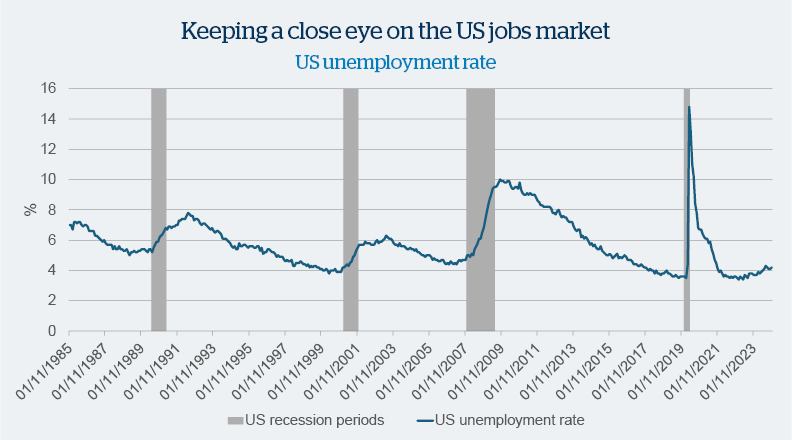

Source: Bloomberg.

This chart shows the unemployment rate in the US over time. For months, we’ve been watching for any cracks in the US labour market, which has been remarkably robust. Even so, we can see that the unemployment rate is rising – albeit at a moderate pace.

While we aim to make the most of the current buoyancy in the economy and financial markets, we’re mindful that the jobs market can turn quite suddenly in recessionary conditions. We’ll continue to watch closely for any signs of change.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are slightly 'overweight' stock markets/shares. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in shares versus our long-term average.

We have slightly shifted the balance of assets held in our multi asset strategies, which has resulted in our strategies holding slightly less in bond market investments than at the time of our last Investment Views update.

Having been a rather uninteresting part of financial markets for quite some time, bond yields rose higher in 2023 than they had done for many years (and bond prices, which always move in the opposite direction to yields, fell). This presented what we perceived to be an attractive buying opportunity.

We still think bonds look attractive over the long-term, with yields at meaningfully higher levels than any point in recent years. However, rising government debt (and the subsequently higher supply of government debt to the market) is among the factors giving us pause for thought.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bonds which is consistent with our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340