Investment Team Handelsbanken Wealth & Asset Management

21 Feb 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Inflation is stabilising, but expect some surprises along the way

Inflation has been heading lower in recent history – welcome news following a period of elevated pricing pressures, amid the shockwaves of the pandemic crisis. New inflation data is released on a regular basis, and the tendency for these regular updates to surprise analysts (by being much higher or lower than expected) has also broadly fallen as inflation has stabilised. However, inflation surprises are creeping up a little in developed economies, and we should probably expect a few more bumps in the road over the coming months.

For example, the UK’s latest inflation reading (measured by the Consumer Price Index, or ‘CPI’) was higher than predicted, at 3% rather than 2.5%. As a reminder, the Bank of England’s target for UK inflation levels is 2%. However, this higher-than-expected January result is unlikely to affect future decisions on interest rates by the Bank of England, as this figure was influenced by a burst of higher prices in areas like food and energy, which policymakers tend to see as mostly near-term noise.

Pressure is mounting for UK interest rate cuts, despite inflation news

The Bank of England is under pressure to reduce interest rates, in order to support economic growth – more so than some of its international peers like the US Federal Reserve. This reflects the UK’s uneasy economic outlook, which is being darkened by uncertainties ranging from the impact of the UK Budget to economic issues in Europe.

Among the Bank’s committee of leading policymakers, support appears to be growing for further interest rate cuts, and we have a long-held suspicion that the Bank will need to do more (in the way of interest rate cuts), and more quickly, than financial markets expect.

Trump’s tactics continue to play havoc with the global outlook

The return of President Trump to the White House means that every assertion we make about the near-term outlook for the global economy must come with a fistful of caveats.

There are regional issues, such as Trump’s approach to the ongoing conflict between Russia and Ukraine. Setting aside the very plain humanitarian and political concerns, Trump’s policies here could have significant knock-on effects for Europe’s economy, including European inflation.

The threat of a tariff war with the US also hangs over various regions, again including Europe. There is little doubt that if tit-for-tat tariffs begin to meaningfully take hold, they will impact economic data, creating the potential for new inflationary pressures as prices are lifted higher by import/export charges. If inflation spikes upwards, it will not be welcomed by either bond or stock market investors. While we can’t account for every eventuality in financial markets, particularly under President Trump 2.0, this is certainly a key risk for investors to manage.

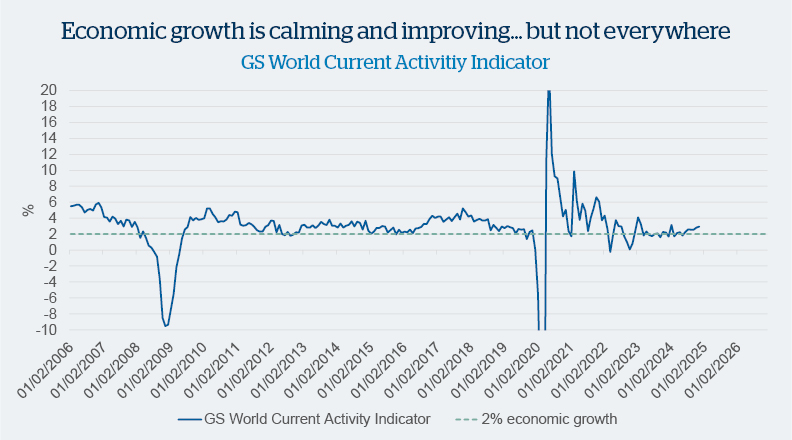

Source: Bloomberg, Goldman Sachs

Global economic growth has been very volatile since the pandemic crisis, but it now appears to be settling down, which is a good thing. Even better, having previously begun to settle at around 2%, global growth now appears to be accelerating slightly, moving into the 3% range.

This resilient growth has contributed to the positive market mood for investors in 2024, and in 2025 so far. However, it’s important to note that much of this growth is a gift from the powerful US economy, rather than being spread out evenly across the global economy, or even developed economies. As the year progresses, this uneven growth will be an area to watch.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are slightly 'overweight' stock markets/shares. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in stock markets versus our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds. Because of their wide variety, it’s difficult to make sweeping statements about alternative assets, and our overall ‘underweight’ stance in this diverse area of the markets hides some specific preferences.

At present, we have a preference for assets which can drive financial returns, without being closely linked to mainstream financial markets. Among our positions in property investments, we have a preference for global assets over UK-based assets, believing that this allows us to access a much more diverse array of property, from data centres to telecoms towers. Other notable positions include a long-term portfolio position in gold, and a specialist hedge fund designed to protect against dramatic market falls.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340