Investment Team Handelsbanken Wealth & Asset Management

16 Jan 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Trump is already setting the tone for his presidency

President-elect Trump has had a vocal start to 2025, announcing an array of characteristically far-fetched plans for his forthcoming second stint in the White House, from annexing Greenland to renaming the Gulf of Mexico.

Among the headline-grabbing noise, Trump has also offered more economically relevant previews into his future presidency, including repeating his commitment to tariffs as a key component of his trade policy. So-called US ‘economic exceptionalism’ also looks set to continue under Trump, as his proposed tax cuts and deregulation are likely to boost an already buoyant US economy.

With these two factors in mind, we’re conscious of the unintended consequences of turbo-charging US economic growth, including the impact on inflation, and what this could mean for interest rates and bond yields. Reflecting this, across our multi asset strategies, we continue to hold a larger amount in US stock markets (which would likely be boosted by economic growth) and a smaller amount in US government bonds (which would likely be hurt by higher inflation) versus our long-term average positions.

Bond market drama strikes again in the UK

Rising bond yields have also held media attention in early 2025, as investors demand more compensation to lend their capital out for the long term. This reflects their fears of higher inflation down the line. While this has led to rising yields across all types of bond markets, government bonds have garnered particular attention.

In the UK, investor concerns about the fiscal discipline of the new UK government have also pushed government borrowing costs (i.e. bond yields) higher. Cuts to government spending may be the way forward, though in our view a contraction in the UK economy is likely regardless. This would push the Bank of England to cut interest rates in order to restimulate economic activity and growth, probably bringing bond yields lower (and bond prices, which always move in the opposite direction to yields, higher).

Within our multi asset investment strategies, UK government bonds feature as the main component of our bond market positions. We reduced some of our exposure here in November, given some concerns following the new government’s Budget. Within our stock market exposure, our UK positions are focused on the shares of large, global businesses whose earnings have little dependency on the domestic UK economy.

A difficult picture for China and Europe

Chinese authorities have left no stone unturned in their efforts to stimulate their economy (in particular the property sector), from interest rate cuts to public spending. Despite all this – and in stark contrast to its developed economy peers – the Chinese economy remains mired in deflation. Falling prices can have meaningful effects on economic growth, holding back household spending and damaging corporate revenues and ultimately leading to weakness in employment markets.

China’s economic woes also represent a challenging backdrop for European businesses whose income depends on Chinese consumers and businesses. Indeed, Europe currently looks weak from an economic perspective, with Germany – Europe’s erstwhile economic powerhouse – struggling amid falling industrial production levels. While overall inflation remains close to the 2% target in Europe, inflation in the services sector is still elevated (much like in the UK). This economic weakness is likely to encourage further interest rate cuts from the European Central Bank.

Against this backdrop, both Europe and China (and by extension developing economies) continue to look unappealing from an investment perspective, in our view. This is reflected in our limited investment positions in these areas.

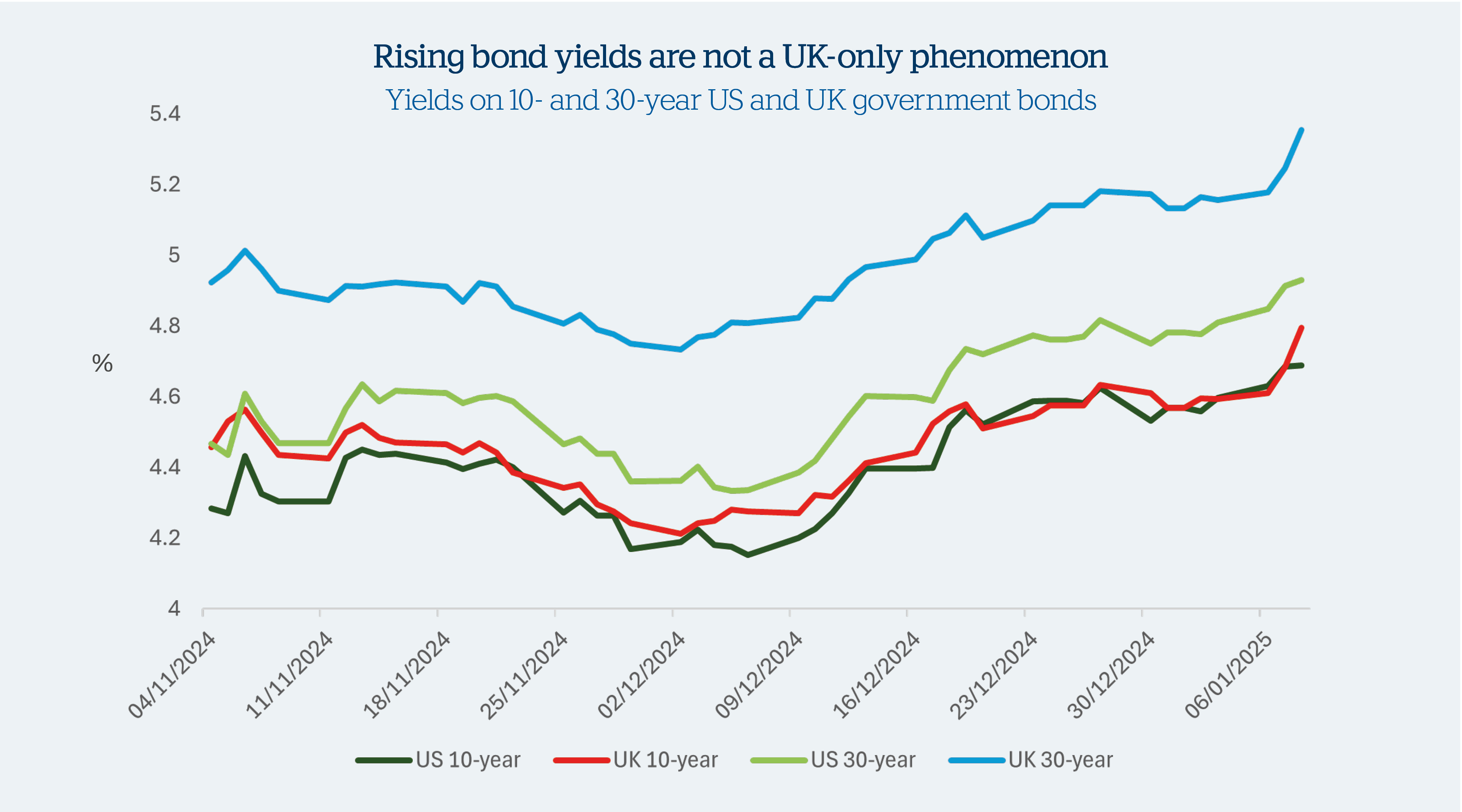

Source: Bloomberg.

UK bond markets held the headlines last week, but bond yields have been rising in most developing economies in recent years. (As a reminder, bond yields move in the opposite direction to bond prices, so bond yields have risen as bond prices have fallen). For example, since September 2024’s low in yields, the yields on UK and US 10-year bonds have effectively moved up in tandem.

This tells us that, while it certainly felt like it in early January, rising bond yields are not in fact a UK phenomenon. At a global level, the cause of higher yields is likely a combination of factors, from the risks of higher inflation under Donald Trump’s next presidency, to the higher government debt levels in developing economies which are spooking investors.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are slightly 'overweight' stock markets/shares. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in stock markets versus our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds. Because of their wide variety, it’s difficult to make sweeping statements about alternative assets, and our overall ‘underweight’ stance in this diverse area of the markets hides some specific preferences.

At present, we have a preference for assets which can drive financial returns, without being closely linked to mainstream financial markets. Among our positions in property investments, we have a preference for global assets over UK-based assets, believing that this allows us to access a much more diverse array of property, from data centres to telecoms towers. Other notable positions include a specialist hedge fund designed to protect against dramatic market falls.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340