Investment Team Handelsbanken Wealth & Asset Management

04 Jul 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Investors want to move on from tariff wars and military conflict

We’ve reached the halfway point of 2025, and there’s still lots going on in the global economy and financial markets.

Markets are nothing if not fast moving, and the brief and brutal escalation of Middle East conflict already appears to be a thing of the past for asset prices. The oil price is now back to levels last seen prior to Israeli’s opening attack on Iran’s nuclear infrastructure. Riskier asset types like shares and corporate bonds were also stronger as June turned to July, signalling a more upbeat mood among investors.

Meanwhile, tariffs – which had been pushed to the back pages of the media – have returned to the front pages once more. The 90-day deadline set by the White House for global trading partners to agree on tariff levels is now expiring. However, we do think these import taxes will mostly end up lower than threatened in President Trump’s original ‘Liberation Day’ announcements on 2 April.

Thinking positive for the second half of 2025

As we write, both tariff wars and military conflict have begun to recede from investors’ view. If this continues, it should provide a helpful setting for financial markets as we enter the second half of 2025.

It’s fair to say that the White House has been at the heart of some of the rockiness impacting financial markets in 2025 so far. The good news is that the White House can also provide some of the solutions. If Trump’s next policies include – as we suspect – more tax cuts and deregulation, we could soon enter the more market-friendly period of his second presidency. Price moves in financial markets indicate that investors believe this era is coming.

How are our investment strategies positioned for the next chapter?

We’ve spent the past 18 months or so simplifying our investment positions and making them exceptionally ‘liquid’ – ready to move easily if need be. Our investment strategies are well-diversified across different types of financial assets, including our stock market positioning, where we’ve previously slightly reduced our exposure to the choppy US market.

Our government bond positions haven’t always been helpful to investment performance in recent history, but now appear to be delivering the better results we’d expect to see in response a stressful global landscape. Meanwhile, the most traditional ‘safe haven’ for investors – gold – has been exceptionally strong in 2025 so far, helping to cushion our investment strategies from some market turbulence. We also have specialist hedge fund positions which are designed to help in times of market stress – we think of these as a kind of insurance policy, which we hope won’t be called upon, but are there to help in the worst of times.

As we’re sure our clients already know, investing always means exposing your capital to the possibility of both rises and falls in financial markets, presenting both risks and opportunities. It’s our privilege to help you understand more about this, so if you would like more information, please do get in touch.

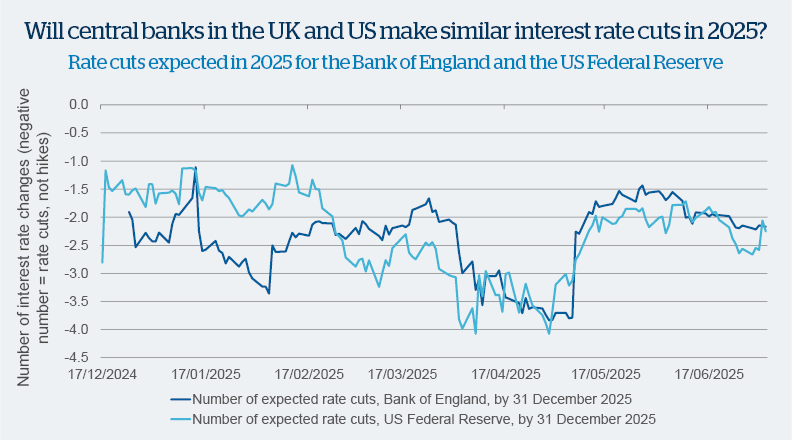

Source: Bloomberg

This chart reflects signals from bond markets, estimating how many times the Bank of England (the Bank) and the US Federal Reserve (Fed) will change interest rates by the end of 2025. (The negative values down the left-hand side of the chart indicate that investors expect rate cuts, not rate hikes.) The chart shows us that investors expect interest rate cuts at the Bank and the Fed to be roughly in step by the end of the year.

However, many factors remain uncertain. Investors will be watching closely for any signs of improvement or deterioration in key economic data, such as employment markets, consumer spending, or economic growth. Political turbulence is also a factor to consider in both countries, as this can impact economic confidence in the short term, leading to delays or changes to central bank decisions. In the UK, the government is grappling with holes in its spending plan, while in the US, President Trump’s administration remains an unreliable force on the domestic and global stage.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are 'neutral' stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340