Investment Team Handelsbanken Wealth & Asset Management

05 Jun 2024 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Economic data suggests that the US economy grew at a rate of 1.3% in the first quarter of 2024 (January to March), dropping from 3.4% in the final three months of 2023. This points to an economy in the process of slowing down, and perhaps moving towards a more sustainable level of economic growth. While it remains to be seen if this trend will continue, these initial signs could provide encouragement for the US central bank, which has been attempting to take the heat out of inflation, using higher interest rates as a tool to contain economic activity. Meanwhile, we still see signs of burgeoning growth in other regions, like the UK and mainland Europe.

The latest updates suggest that pricing pressures are continuing to fall back in key economies. For example, the final week of May saw the release of Personal Consumption Expenditure (or ‘PCE’) figures for April – this is the US central bank’s preferred measure of inflation, and the figures showed that inflation had slowed to its lowest rate in 2024 so far. As a reminder, this does not mean that the costs of goods and services fell in April, but that prices were increasing at a slower rate. It’s still reasonable to expect bumps in the road for the journey away from higher inflation, but signals like this are certainly encouraging for central banks, and for investors hoping for interest rate cuts in the near future.

In recent history, investors have commonly assumed that interest rates would be cut on this side of the Atlantic (in the UK and Europe) before the US central bank made its first move, with the Bank of England’s June meeting touted by analysts as the possible starting point for cuts. However, the announcement of a UK general election on 4 July has created fresh uncertainty about the timing of future UK interest rate cuts: the Bank has cancelled all press conferences from now until after 4 July, pushing investor expectations for the first UK interest rate cuts back to the Bank’s August meeting.

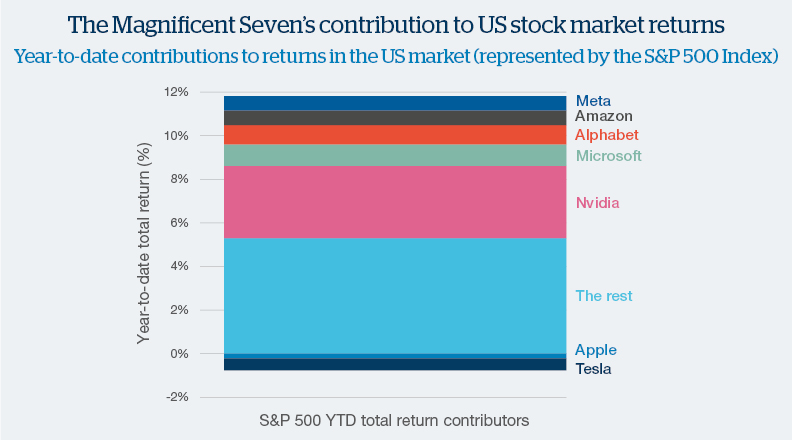

Source: FactSet, data to 23 May 2024, measured in US dollars.

If you’ve been following financial market news in 2024, you might have heard of the ‘Magnificent Seven’ – a set of ultra-large US businesses which have been dominating stock market performance. The chart shows us just how much the shares of the Magnificent Seven have contributed to US stock market returns so far in 2024: around 50%.

However, the bulk of these returns have come from just one technology giant: Nvidia. This is an extraordinary level of dominance from one single company, and demonstrates the very shallow pool of big winners in the US market today, as well as highlighting the importance investors currently place on the artificial intelligence theme.

We’ve recently slightly increased our stock market positions to reflect our view that we are approaching the later stages of a period of recession. We achieved this by reducing our positions in a number of other market areas, most notably alternative asset types and debt in developing economies.

Within our stock market positions, we favour the shares of smaller and mid-sized businesses, as well as positions in healthcare, insurance and clean energy. With a few key exceptions, we currently prefer to limit the bulk of our stock market exposure to developed economies.

At the time of this update, we are 'neutral' when it comes to stock markets/shares. This means that we have not deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

Our multi asset investment strategies currently hold a higher proportion of assets in ‘fixed income’ markets (like government bonds) versus our long-term average positions. Having been a rather uninteresting part of financial markets for quite some time, bond yields rose higher in 2023 than they had done for many years (and bond prices, which always move in the opposite direction to yields, fell). This presented what we perceived to be an attractive buying opportunity.

Building up our bond exposure has meant not only increasing the proportion of bonds that our strategies hold, but also the maturity of these bonds, particularly UK government bonds. Adding longer-maturity bonds gives us a greater sensitivity to movements in expectations for interest rates, and we continue to believe the market is underappreciating how much the Bank of England in particular will cut interest rates over the next 12-18 months, despite potential delays in starting this process due to the general election.

At the time of this update, we are slightly 'overweight' bond market investments. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in bonds versus our long-term average.

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds. Because of their wide variety, it’s difficult to make sweeping statements about alternative assets, and our overall ‘underweight’ stance in this diverse area of the markets hides some specific preferences.

At present, we have a preference for assets which can drive financial returns, without being closely linked to mainstream financial markets. Among our positions in property investments, we have a preference for global assets over UK-based assets, believing that this allows us to access a much more diverse array of property, from data centres to telecoms towers. Other notable positions include a specialist hedge fund designed to protect against dramatic market falls.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340