Investment Team Handelsbanken Wealth & Asset Management

06 Jun 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Coming into May (a month after tariffs were imposed), the global economy was in so-called ‘stall speed, with GDP growth of around 2%. In economic growth terms, this is neutral gear, or treading water.

A peek below the surface revealed a mixed assortment of economic signals as May began. Let’s take the US – the world’s most dominant economy – as an example, as what happens in the US affects the rest of the world too. On one hand, flagship measures of US economic health, like data from employment markets, had been holding up surprisingly well. On the other hand, US consumers (the driving force behind the US economy) were feeling decidedly downbeat, according to national survey data covering April.

As May progressed, a springtime feeling appeared to work its magic. By the end of the month, US consumers broke away from five straight months of feeling downbeat about the US economy, returning to positivity. Other optimistic economic signs came from a range of sources, such as quite robust news on US business earnings (in reports covering the first three months of the year), and – on the global front – improving export data among some crucial Asian trading hubs.

Some progress in resolving Trump’s tariff wars added to the upbeat mood. It’s worth noting, though, that with court cases pending and many would-be trade deals still outstanding, we’ll probably see a few more twists and turns on the road ahead when it comes to agreements with America’s global trading partners.

For now, asset prices have generally recovered quite well (and quickly) following their weakness earlier in the year. Nevertheless, the mood among investors is still vulnerable to surprises, and a punchy policymaker (President Trump) is still at the helm of the world’s most powerful country. Even as we write, his vicious public spat with former close adviser (and CEO of Tesla) Elon Musk is making price waves in the US stock market.

We’re watching carefully for the next moves from the White House. Trump’s presidency may have begun with market-unfriendly tariff wars, but we still expect more market-friendly policies ahead, such as government spending and deregulation.

For financial markets, there is always the possibility of rises and falls, presenting both risks and opportunities for investors. We believe this supports our multi asset, global approach to investing, but if you’re feeling nervous about the recent events in financial markets and would like more information, please do get in touch.

Source: Macrobond

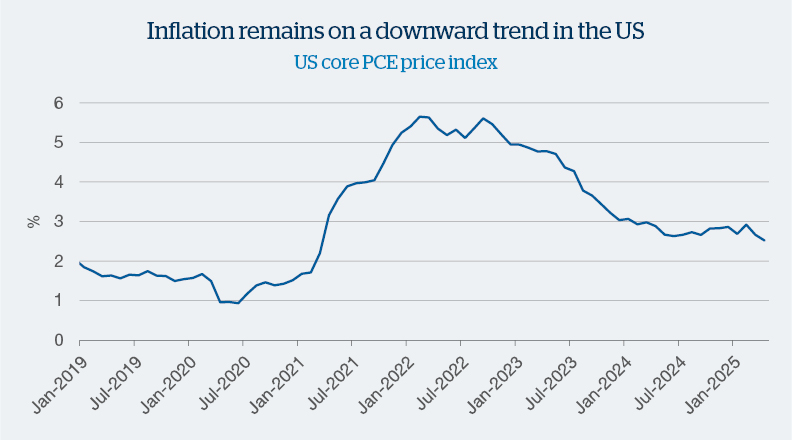

The Personal Consumption Expenditures price index – or ‘PCE’ – is a measure of inflation. In fact, it’s the US Federal Reserve (the US central bank)’s preferred way of measuring inflation. The chart above shows us that ‘core’ PCE (which excludes the prices of food and energy) has been on a downward trend in recent months, following the heights reached a couple of years ago. (As a reminder, falling inflation does not mean that prices are falling – it means that prices are rising more slowly than before.)

When inflation spiked higher in very recent history, leading central banks around the world hiked up interest rates to try to slow down economic activity and cool down pricing pressures. This appears to have done its job, and signs of falling inflation should encourage central banks to allow interest rates to move lower again in the coming months. Trump’s tariff wars could be a potential fly in the ointment, should they lead to fresh inflationary pressures – this is one to watch.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are 'neutral' stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340