Investment Team Handelsbanken Wealth & Asset Management

19 May 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

The world of trade has been turned upside down

Since President Trump’s re-entry to the White House, global trade as we know it has been turned on its head. This is the biggest shock to trade since the 1970s, when the Bretton Woods system – designed to encourage long-term global growth and help countries recover following WWII – collapsed. In fact, the tariffs proposed by Trump, would have put trade barriers (in the form of taxes) at their highest levels since the early 1900s.

Despite his repeated earlier threats to introduce higher trade tariffs, Trump’s opening gambits were much more extreme than expected, causing financial markets to scramble to reflect this new world order in asset prices.

This chaotic experience also taught us something new, though. In his first presidency, Trump appeared to see the performance of the US stock market as the measuring stick for his success; this time around, it looks like the president’s pressure point could be bond markets. Once bond investors began to penalise US government bonds in earnest, a 90-day tariff negotiating window quickly emerged.

If you’d like to find out more about the impact of Trump’s return to the presidency on the global economy, financial markets, and our investments, you can read our special Insight: 100 Days of Trump.

Taking a long-term view today feels difficult, but essential

The noise of Trump’s second presidency – on so many fronts at once – has been overwhelming. However, we are long-term investors, so it’s our job to look through this short-term chaos and plan for the long run.

We know that tariffs are here to stay, but our hunch is that they will generally settle at lower levels than Trump initially announced. Indeed, this has already begun to happen. Even so, it’s worth noting that – if the example of the UK is anything to go by – this still probably means that we need to acclimatise to a world where trading taxes are higher than we’ve all grown used to.

What are we expecting next?

Very tentatively (and leaving ourselves plenty of room to manoeuvre), we’re operating on the assumption that although we’re likely to see some economic impact from the new tariff levels, we’re also likely to see more economically friendly (and financial market friendly) policies from Trump’s administration as the year progresses. This could include tax cuts and deregulation – Trump took huge swings at these areas during his first presidency, but could still do more. At the moment, our best guess is that these types of policies could start to emerge in the second half of 2025.

Meanwhile, central banks are still sending signals that interest rates are heading lower, and we continue to expect further interest rate cuts from both the Bank of England and the US Federal Reserve as 2025 progresses. Taken altogether, along with a rather large pinch of White House salt, this points to better news for asset prices in the months ahead.

If you’re feeling nervous about the recent events in financial markets and would like more information, please do get in touch.

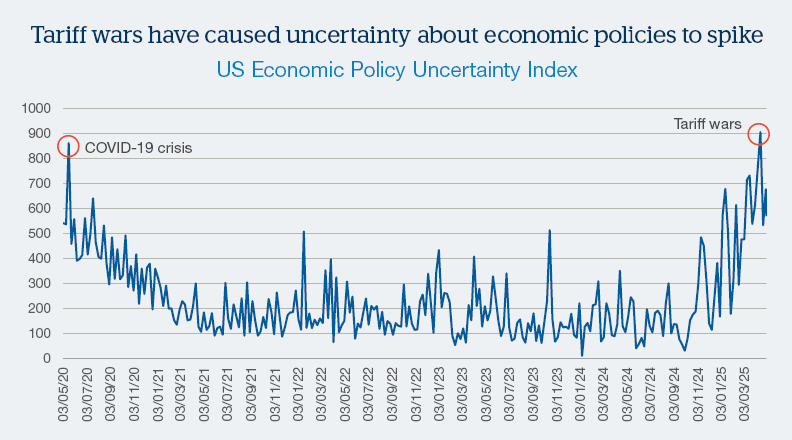

Source: Bloomberg (weekly data)

This chart shows that Trump’s tariff announcements fuelled a huge spike in uncertainty about US economic policies. You can see clearly that the last time uncertainty spiked upwards so strongly was during the early days of the COVID-19 pandemic, when governments across the world stampeded to react to a hitherto unknown crisis.

Financial markets do not enjoy uncertainty, and reacted accordingly. As the market mood begins to cautiously stabilise, we’re biding our time, making only careful adjustments to our investment strategies.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are 'neutral' stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340