Investment Team Handelsbanken Wealth & Asset Management

09 May 2024 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Green shoots of economic recovery are tentatively appearing in regions like Europe and the UK following a period of relatively mild recession. This includes early signs of improvement in the manufacturing sector and credit markets. The picture is slightly different in the US, where despite some very recent slightly weaker employment figures, a surprisingly robust jobs market has helped to keep economic activity quite buoyant over the past couple of years. (Similar decoupling is also apparent between developing countries, with China’s economy faltering while the Indian economy thrives.)

In response to concerted efforts by the world’s leading central banks to bring inflation to heel (by raising interest rates to slow down economic activity), pricing pressures have been falling back in recent months. However, the journey down from multi-decade highs for inflation was never likely to be smooth, and pockets of stubborn pricing pressures have persisted, such as in areas like housing. This is a challenge for central banks, who must decide when (and by how much) to begin lowering interest rates. If they move too soon, they could endanger the move away from higher inflation; move too late, and they could damage the growth of the economy.

In the opening months of the year, investors have been assessing this challenging economic landscape, and trying to chart a way through it. In practice, this has meant revisiting (repeatedly) expectations for the timing and scale of interest rate cuts from leading central banks in 2024. Back in January, hopes were high that the first interest rate cuts would begin in spring, before being peppered throughout the rest of the year. Stubborn inflation has tempered these expectations: investors still expect interest rate cuts this year, but not at the pace and magnitude previously envisioned. It’s now widely expected that interest rates will be cut on this side of the Atlantic (in the UK and Europe) before the US central bank makes its first move.

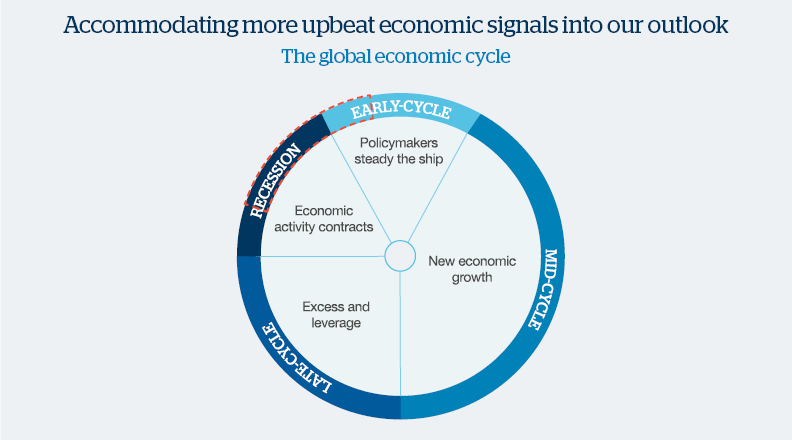

Source: Handelsbanken Wealth & Asset Management

This chart shows the global economic cycle – the regular fluctuations between periods of growth (expansion) and recession (contraction). The highlighted segment represents our outlook for the coming 12-month period.

We are encouraged by green shoots of recovery emerging (in areas like credit markets and the manufacturing sector), alongside a sense that the global growth is acclimatising and inflation normalising. This has led us to feel quietly and cautiously optimistic. As a result, we have slightly shifted our outlook for the global economy from recession towards ‘early-cycle’.

At the time of this update, we are 'neutral' when it comes to stock markets/shares. This means that we have not deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are slightly 'overweight' bond market investments. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in bond versus our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.