Investment Team Handelsbanken Wealth & Asset Management

12 Sep 2024 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Economic growth continues to disappoint, and it’s a global issue

If the latest economic data is anything to go by, the green shoots of economic growth visible in early summer could now be fading – though only time will tell.

At the time of writing, the all-important US economy is still growing, but the pace of this growth has slowed dramatically. On the heels of a very brief recovery, the US manufacturing sector is now contracting again.

Meanwhile, growth is stuttering in China, and in Germany – the key European powerhouse.

Central banks have wrestled with inflation, but now unemployment has entered the ring

As the world’s leading central bankers look poised to declare victory over inflation, their focus now shifts to employment markets. In particular, as US employment shows increasing signs of strain, the US Federal Reserve (Fed) grows evermore mindful of its dual mandate: the central bank is tasked with not only keeping inflation at a manageable level, but also keeping a lid on the unemployment rate.

Over the past couple of years, we’ve often noted that the interest rate hikes enacted by central banks around the world would work with a lag – their true effects only felt some time after the hikes were made. The same is true of the interest rate cuts which have now begun in all major regions besides the US (which has signalled a September rate cut). We will need to wait some time before the impact of these cuts feeds through into the economy.

Markets have had a changeable summer, so what next?

August was marked by high levels of market volatility, with share prices dropping sharply early in the month. Investors were responding to weaker economic data and disappointing news on company earnings from some US tech giants. Stock markets stabilised as the month went on, as investors regained some of their confidence, buoyed by a strong indication that the Fed would begin cutting rates in September.

With the first Fed rate cuts since 2020 on the horizon, markets will be watching closely for anything that could influence the path of future rate cuts from here, and any clear signals of impending economic downturn. As the old adage goes: when the US sneezes, the world catches a cold. Investors will be watching closely for any signs of an American sniffle.

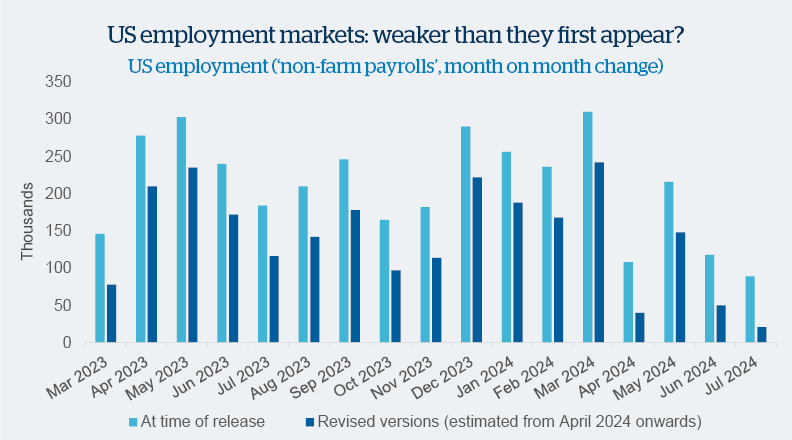

Source: Bloomberg. Revised versions from April onwards assume the same monthly revisions as those seen over the previous 12 months.

When US employment data is first made public, an initial version is released to begin with, followed by a subsequent, updated revision. This chart shows both sets of data. The light blue bars show the initial version of the data, while the dark blue bars show the later revisions.

It’s worth considering the challenges this presents for the US central bankers in charge of making decisions about how to support employment markets. Over the past few months, the true picture of unemployment has been consistently weaker than policy decisions may have taken into account. This increases the risk of a policy error from the Fed, such as waiting too long to make cuts to interest rates. The Fed is expected to cut rates this month, but if this is already too late, the delay could have a greater negative impact on consumers – the driving force behind the US economy.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

We favour the shares of larger businesses, as well as positions in healthcare, insurance and clean energy.

With a few key exceptions, we currently prefer to limit the bulk of our stock market exposure to developed economies.

At the time of this update, we are 'neutral' when it comes to stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

Our multi asset investment strategies currently hold a higher proportion of assets in ‘fixed income’ markets (like government bonds) versus our long-term average positions. Having been a rather uninteresting part of financial markets for quite some time, bond yields rose higher in 2023 than they had done for many years (and bond prices, which always move in the opposite direction to yields, fell). This presented what we perceived to be an attractive buying opportunity.

Building up our bond exposure has meant not only increasing the proportion of bonds that our strategies hold, but also the maturity of these bonds, particularly UK government bonds. Adding longer-maturity bonds gives us a greater sensitivity to movements in expectations for interest rates, and we continue to believe the market is underappreciating how much the Bank of England in particular, will cut interest rates over the next 12-18 months.

At the time of this update, we are slightly 'overweight' bond market investments. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in bonds versus our long-term average.

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds. Because of their wide variety, it’s difficult to make sweeping statements about alternative assets, and our overall ‘underweight’ stance in this diverse area of the markets hides some specific preferences.

At present, we have a preference for assets which can drive financial returns, without being closely linked to mainstream financial markets. Among our positions in property investments, we have a preference for global assets over UK-based assets, believing that this allows us to access a much more diverse array of property, from data centres to telecoms towers. Other notable positions include a specialist hedge fund designed to protect against dramatic market falls.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340