Investment Team Handelsbanken Wealth & Asset Management

12 May 2023 8

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Well-publicised recent issues in the banking sector have added an air of nervousness to some areas of financial markets. Since the start of the year, four banks have failed, three of which were based in the US. We know that events like this are unsettling, least not because they bring to mind the 2008 financial crisis. However, it’s important to note that this is not 2008, which played host to a catastrophic chain of events centred on credit (debt) markets. Today, the problems facing some banks have more to do with liquidity (the ease with which assets can be bought and sold), rather than credit.

In many ways, these current issues demonstrate the lagged effects of interest rate rises at central banks, which have exposed some vulnerable institutions unable to service their liabilities in these conditions. Unfortunately, some casualties were inevitable as the knock-on effects of a higher interest rate regime were slowly digested. Importantly, we do not believe that these banking failures indicate signs of deep-rooted distress in the banking sector.

Nevertheless, these events will have an impact on bank lending, with lending standards becoming more restrictive, particularly for riskier borrowers. Surveys of smaller businesses indicate that borrowing conditions are already very tight – perhaps their tightest in a decade – meaning that it is now more difficult/expensive for some smaller or riskier businesses to borrow from their banks. Again, this doesn’t mean we’re expecting a ‘credit crunch’ scenario, as in 2008, but it does mean that we are likely to see a gradual reduction in economic activity as businesses struggling to borrow begin to simply do less. This plays into the hands of central banks, who are actively trying to reduce economic activity in order to rein in inflation.

As banks reduce the amount of credit available to businesses and consumers, inadvertently restricting economic activity, this is likely to do some of the work for central banks. In turn, this could lessen the need for policymakers to continue hiking interest rates quite so aggressively as in the recent past.

From our current vantage point, it’s difficult to predict where the precise end point will be for interest rate rises, but we continue to believe that central banks are closer to the end than the beginning of the current set of rate hikes. In the first half of 2023, we think that the US Federal Reserve Bank (Fed) will have stopped raising interest rates. Indeed, financial markets are predicting interest rate cuts from the Fed in the second half of this year, but we think this is probably premature: central banks have staked their credibility on taking the heat out of inflation, and – all else being equal – they won’t lower interest rates until they’re absolutely sure the job has been done. Once they’ve stopped hiking, we think the Fed will hold interest rates steady for some time in order to monitor the economic environment.

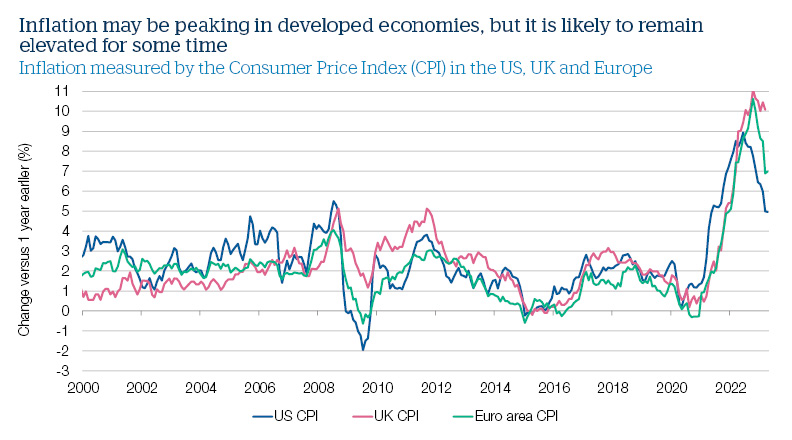

Inflation appears to have already peaked, or at least be hovering around its peak, in most major economies. A number of factors have helped pricing pressures to ease, including the falling back of energy prices and the normalisation of previously embattled supply chains. Recent economic data has also been broadly softer, albeit a number of readings have continued to positively surprise analysts. Though it sounds perverse, weaker economic data is part of the goal for central banks across the developed world. To reiterate: reducing economic activity should help to bring down inflation.

Even so, despite some encouraging signs, inflation is likely to remain elevated for the foreseeable future. This is due to a range of influences, including stubbornly rising US wages and ongoing price rises in the service sector. We continue to watch economic, industry and market data very closely for signs of change.

Source: Macrobond and National Sources

In recent months, we have been reducing the relative prevalence of riskier asset types like shares and alternative assets (i.e. assets outside of traditional bond and stock markets) within our investment strategies. This has reflected our belief that there are better opportunities elsewhere in financial markets, including in bond markets.

Below, we have highlighted some of the key convictions currently at work in our strategies.

Remaining cautious about stock market valuations

We still believe that share price valuations remain unduly elevated, based on overly optimistic predictions for company earnings this year. Given the weaker economic outlook, we think earnings will struggle to meet market expectations of 2% earnings.

Against this backdrop, bond markets look more attractive, and for the first time in a long time are providing a real alternative to stock markets for investors.

Making our investment strategies more defensive

Since our last Strategy Update, we have tilted our stock market holdings towards more defensive areas (such as reducing UK shares in favour of global healthcare shares). Where appropriate, our strategies have also topped up their positions in a specialist hedge fund designed to protect against very sharp market falls.

Now, we are also adjusting our government bond holdings, increasing ‘duration’ (the responsiveness of a bond’s price to changes in interest rates), and reducing our exposure to high-yielding, higher risk corporate bonds.

Upholding our preference for small and mid-size businesses

We retain our preference for the shares of smaller and mid-sized businesses versus their larger counterparts. So far this year, this has not been rewarded, as stock market performance has been dominated by a tiny number of very large businesses, such as tech giants like Apple and Google (which trades under the name ‘Alphabet’).

However, our sector preferences (positive towards technology shares, and more limited exposure to energy shares) has been helpful.