Investment Team Handelsbanken Wealth & Asset Management

15 Sep 2023 8

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Since early this year, our view has been that we are heading towards an economic slowdown for the global economy, and this view has not changed. We maintain our belief that full effects of central bank actions taken in recent history (i.e. sharp interest rate rises) are likely to hit the global economy with a delayed impact over the coming months.

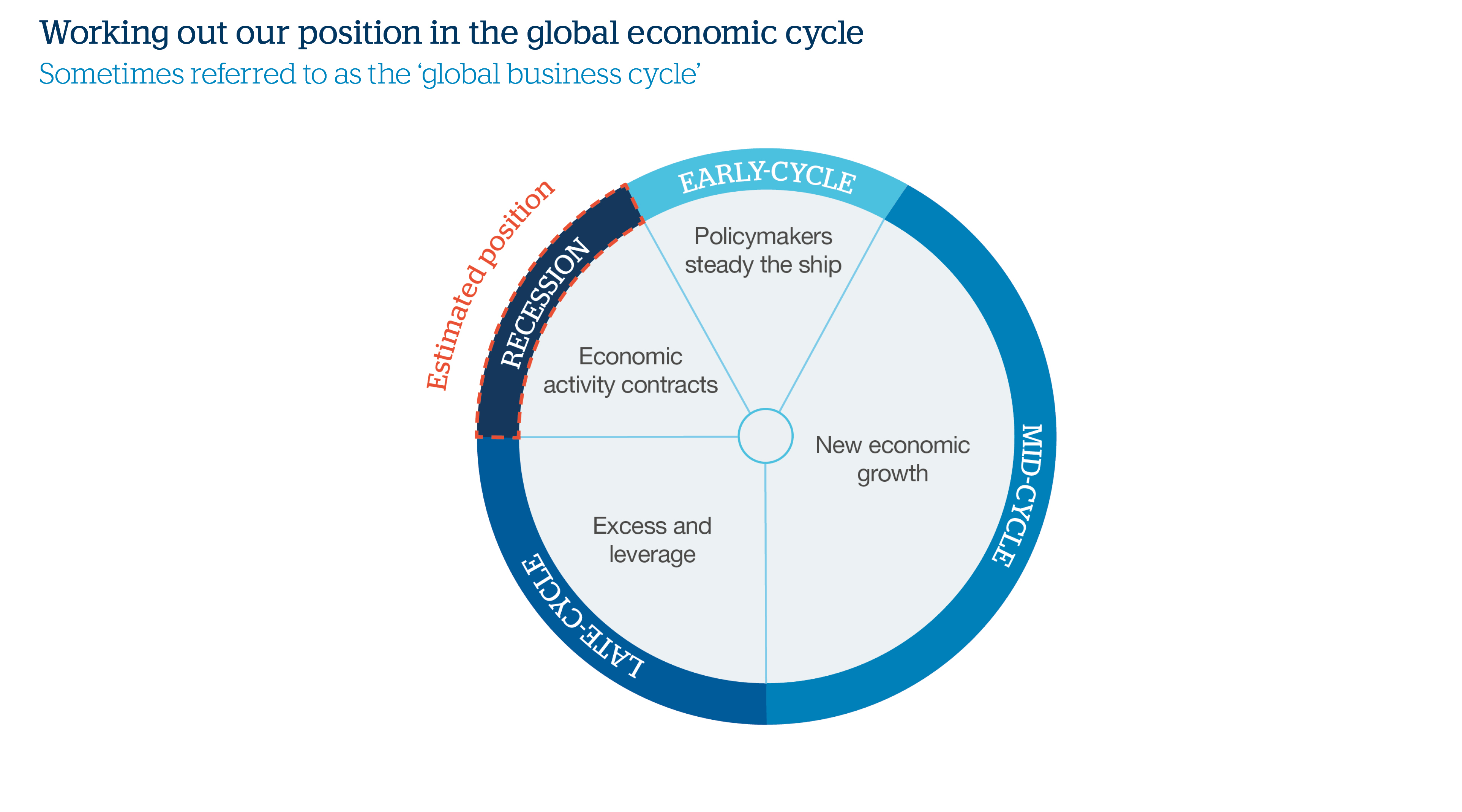

At present, we believe we are in the recession phase of the global economic cycle. As a reminder, there are four phases in the economic cycle, characterised by a slowdown in economic activity – the final phase before the cycle begins anew.

Source: Handelsbanken Wealth & Asset Management

Working out which phase of the cycle we are in today – and how soon the next phase will arrive – is not an exact science, but it matters significantly to our decision making process. This is because it helps us to determine the mixture of different assets at work within our investment strategies, and therefore the level of risk (and types of risk) we are taking on board on behalf of our customers in search of financial reward.

We believe that the global economy is on course to enter a period of downturn in late 2023/early 2024. In keeping with this view, our multi asset investment strategies currently hold a higher proportion of assets in fixed income markets, like government bonds, versus our long-term average positions.

History is never the most reliable guide to future performance, but broadly speaking, as the economic backdrop worsens, bond yields should fall and bond prices (which always move in the opposite direction to yields) should rise. In turn, this would benefit our investment strategies.

Overall, inflation is falling. However, this masks stubborn patches of still-high pricing pressures, such as higher wages, which have played a part in keeping inflation elevated.

It’s also important to remember that while inflation may be falling, it doesn’t move up and down in straight lines. The effects of very high energy prices in 2022 mean that a number of 2023’s inflation readings (comparing prices versus the same period in the previous year) could have been flattered into looking a little lower than they might otherwise have appeared. Overall, we believe the trajectory will be downwards, but there could be some temporary bumps higher over the coming months.

We invest globally, which means that we monitor a wide range of signals from all areas of the world economy. However, given the unparalleled prominence of the US on the global stage – in both economic and stock market terms – we especially keep an eye on signals from across the Atlantic.

The US economy has held up surprisingly well over the past couple of years, despite sharp interest rate hikes from the US central bank designed to take some of the heat (inflation) out of the economy by slowing down economic activity. Indeed, key areas of the US economy have been stubbornly resilient to the central bank’s efforts to slow down economic activity. Among these is the US employment market – despite some nascent signs of slowing down, we still see some areas of undeniable strength. Nevertheless, we’re confident that central bank policies will soon come home to roost for employment markets too. As we mentioned earlier, interest rate hikes impact the real economy with a lag, and our view is that the true impact of central bank policies will hit home over the coming six months.

What’s more, the US economy is driven to a large degree by the power of US consumers, who have maintained a high level of spending in recent history, despite interest rate hikes. They’ve managed this by dipping into the cash they built up during the lockdown era, but these excess savings have now been eroded away. In addition, student loan repayments – which had been put on hold for around three years – have now begun again, giving a large chunk of US consumers even less free cash to play with. Watch this space.

We have not made any significant changes to the positions held in our investment strategies since our last Strategy Update in July. While we made an early decision to increase our bond positions, we are now well positioned for the growth slowdown which we anticipate towards the end of this year and/or the beginning of 2024.

We continue to see attractive opportunities in government bonds

Having been a rather uninteresting part of financial markets for quite some time, bonds are now offering much higher yields than they have done for many years.

Our strategies currently hold a higher proportion of assets in government bonds versus our long-term average positions. We believe that the true benefit of these positions should kick in over the coming months, once (as we predict) economic data begins to worsen and/or the messaging from central banks on the economic outlook becomes more negative.

Against this backdrop, stock markets present less of an opportunity

When we deemphasise a particular asset type within our investment strategies, it doesn’t necessarily mean we feel very negative about that area of the market. Rather, it can mean that we see relatively better options elsewhere.

This is partly the case at the moment for shares within our portfolios, which we have reduced in favour of bonds. However, we also believe that stock markets will struggle as the economic cycle morphs into recessionary conditions.

Feeling neutral about ‘alternative’ asset types

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds.

Because of their huge variety, it’s difficult to make sweeping statements about alternative assets. We are roughly ‘neutral’ about alternative assets overall, but would note that this headline neutrality hides some specific preferences, such as a preference against UK property.