Wealth Team Handelsbanken Wealth & Asset Management

08 Mar 2024 6

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

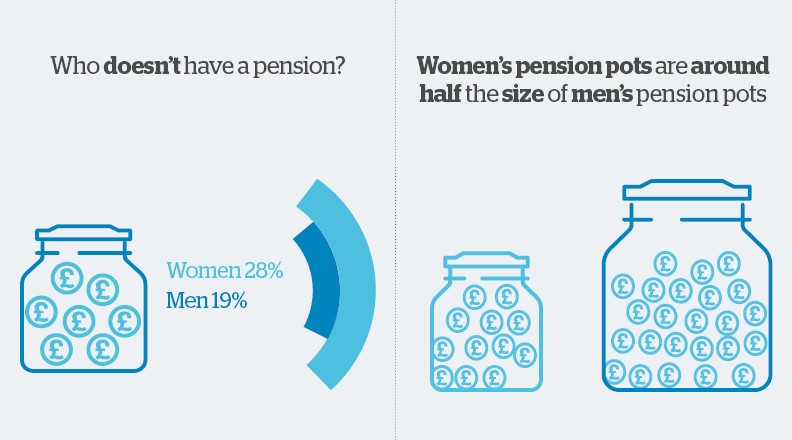

According to this year’s Wealth Survey, three quarters of us have a pension, with an average pot of £272,045. In keeping with last year’s results, women are still less likely than men to have a pension, though this improves among younger age groups. Women over 40 are generally less likely to have a pension than men of a similar age (71% of women versus 83% of men), whereas this is more equal among people in their 30s.

However, among women who do have a pension, their savings are typically much smaller. This year, our survey told us that the average (median) pension pot for a woman is roughly £37,500 – half the size of the average (median) male pension pot of £75,000.

Source: Handelsbanken Wealth & Asset Management Wealth Survey 2024

Most people’s pension savings are tied to their income, whether this is because it defines how much they can afford to contribute to a private pension, or because their workplace pension is linked to their salary one way or another. With this in mind, perhaps it shouldn’t come as a surprise to hear that women’s pension pots are typically much smaller than men’s.

But isn’t the gender pay gap narrowing? In some ways, yes, but unfortunately there is still some way to go. While average hourly wages for younger men and women (18-21 years old) are now roughly even, a pay gap starts to emerge quite quickly as people age. According to Office for National Statistics data, the wage gap between men and women is highest for those aged over 60 years, but even among relatively younger age groups, there has been a worrying creep up in recent years. Over the past few years, the wage gap between men and women for workers in their 20s and 30s has risen back up to levels last seen over a decade ago.1

We can only speculate about the cause of this, but it’s hard to ignore the potential effect of the COVID-19 pandemic on the workforce in general, and on people’s career choices individually. Recent UK labour market statistics have highlighted that the UK workforce has shrunk, with many people leaving the workforce completely in recent years. We know that some of this is sadly due to ill health, but it’s difficult to ignore the gendered wage gap data for workers in their 20s and 30s – the most common age for people to raise children.

Christine Ross, Client Director at Handelsbanken Wealth & Asset Management, suspects this is no coincidence, and worries about the effect this could have on many women’s retirement savings:

“As businesses call upon their staff to return to the office environment, are women in their 20s and 30s resisting? Perhaps they want to maintain the more flexible time with their family that they’ve experienced over the past few years. Or maybe – in this era of high costs of living – they simply can’t afford the extended childcare they’d need to return to higher paying or full time roles.

“Whatever the cause of the increased gender pay gap within these age groups, given the strong link between incomes and pension contributions, this is a very concerning picture for many women’s longer-term finances.”

Perhaps surprisingly, our Wealth Survey didn’t show family or childcare among the top factors people imagined would cause them to take a break from pension contributions. A fifth (20%) of our respondents did expect to take a longer break from making pension contributions, averaging an expected 9 years when they foresaw that they would not be paying into their pension pots.

The main reasons given for this were travel (21%), and health reasons (18%) – the latter is naturally far more worrying given the recent UK labour market statistics on losing workers to ill health. Around 16% of those surveyed thought they would take a break from contributing at some point because they would have accumulated enough wealth and would no longer need to work, while the same number (also 16%) – at the opposite end of the scale – imagined that they would need to take a break from paying into their pensions due to affordability reasons.

Given the UK’s spike upwards in the cost of living, Christine is not surprised to hear this, but she does caution against deprioritising your pension savings if at all possible:

“We know that there is currently a huge amount of competition for our financial resources. More immediate concerns like a higher cost of living and increased mortgage payments are making it really challenging for many people to maintain regular pension contributions.

“Even acknowledging these challenges, it would be irresponsible of us not to point out that making up for any lost pension contributions further down the line can be really tricky. If you find yourself unable to save for retirement at the moment, we’d really encourage you to take some professional advice to build a long-term financial plan. It might seem like a contradiction in terms to pay for help when you’re trying to save money! But it could save you from an expensive misstep.”

When we asked our survey respondents about who was involved in managing their pension, the most common answer was their workplace (38%). Under UK law, all employers must offer a workplace pension scheme. However, according to our Wealth Survey results, only 36% of people felt that their employer was helpful in explaining their workplace pension and post-retirement planning.

As Christine notes, this lack of information from employers can be especially problematic if coupled with a lack of engagement from pension scheme members (employees).

“Usually, there will be lots of different investment options within a pension scheme, but most members will simply stick with the default option. This may not offer the right level of risk and potential financial reward that best fits with their retirement aspirations.

“We see this disengagement in particular with younger pension savers, for whom retirement feels a very long way off, especially once set against other competing near-term financial priorities. This is really unfortunate, as the contributions they make to their pension savings in the earliest years will be given the longest time to attract investment growth. Younger people will also have a very different experience of retirement planning to older generations, who were much more likely to benefit from ‘defined benefit’ or ‘final salary’ pension schemes.”

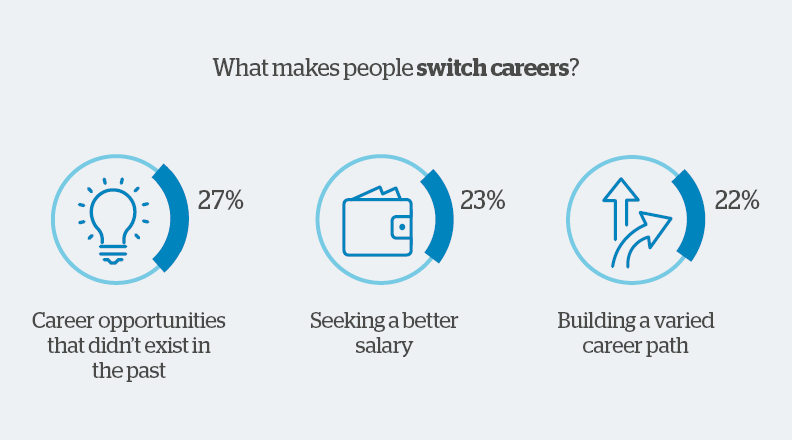

With workplace pensions in mind, how could career changes affect people’s retirement savings? According to our Wealth Survey, most people have had an average of two careers so far – this means working in two distinctly different industries or career paths. Those who have not yet retired expect to average three different careers over their lifetime.

Source: Handelsbanken Wealth & Asset Management Wealth Survey 2024

While career changes can present fantastic opportunities (personal and financial), Christine is keen to highlight that switching industries could mean facing up to some pension-related risks:

“Restarting in a new industry, or returning after an extended break, can feel like entering the workplace for the first time all over again. If you’re moving to a self-employed role having previously enjoyed the benefits of a workplace pension scheme, can you afford to make private pension contributions? If your new role includes a workplace pension scheme but offers a lower salary (likely lowering the amount paid into your workplace pension), can you make up the shortfall? These considerations needn’t stop you from branching out into exciting new careers, but they should feature in your financial plan.”

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340