8

Important changes to your tax reporting responsibilities to HMRC

Following several setbacks and delays in recent years, from 6 April 2026 HMRC will finally press ahead with the next phase of its digital transformation of the UK tax system.

HMRCs ‘Making Tax Digital for income tax’ is a new system for recording and reporting income and expenses if you are self-employed and / or receive property income. The new rules will be phased in over the upcoming 2026/27 and 2027/28 tax years.

- From 6 April 2026, taxpayers with gross income of over £50,000 from self-employment and/or property will be within the scope of the new rules, and

- From 6 April 2027, those with gross income over £30,000 from self-employment and/or property income will also be caught.

- From 6 April 2028, taxpayers with annual gross income of between £20,000 and £30,000 from self-employment and/or property will be brought into the new system.

For the purposes of determining whether the new rules apply to you, ‘gross income’ refers to the combined gross income received from self-employment and/or property and not your ‘net’ or taxable profits after the deduction of allowable expenses.

The new rules are mandatory and will be phased in from 6 April 2026. We understand that HMRC will be writing to those taxpayers who they believe will be impacted in April 2025.

What will happen from 6 April 2026?

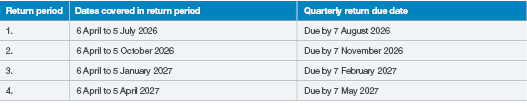

From this date, if your income from self-employment and/or property exceeds £50,000 per year, you will be required to submit quarterly updates to HMRC in accordance with the following table:

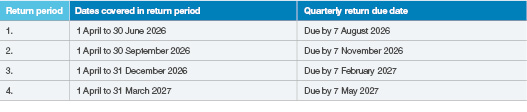

Alternatively, it will be possible to elect for the quarterly periods to tie in with a month end if this is more convenient, per the table below:

As can be seen, the due date for the submission of each quarterly update will be the 7th day of the following month or the month after the following month, if you elect to run your quarterly updates to the month end. The periods covered will be cumulative and so each quarterly update will effectively supersede the previous one.

Each quarterly update must include details of the self-employed and/or property income received, together with the allowable expenses incurred, in that period.

Details of any other taxable income or capital gains will not be reportable through the quarterly updates. Instead, a ‘final declaration’ will be required to provide HMRC with details of the final taxable profit(s) for the period, together with any other taxable income and capital gains arising in the tax year.

Submission of the final declaration (by 31 January 2028 for those brought within the rules from 6 April 2026) will complete the quarterly update process for 2026/27 and will supersede the requirement to submit an annual tax return through Self-Assessment.

What will happen from 6 April 2027?

If your income from self-employment and / or property exceeds £30,000 you will be required to submit quarterly updates to HMRC as outlined above. The first quarterly update will be due by 7 August 2027 and so forth.

Will I need to pay tax on a quarterly basis?

No.

As matters currently stand, the government has not announced any plans to require taxpayers to make quarterly tax payments on account. However, in our view, this possibility cannot be ruled out at some point in the future once the new quarterly update system is successfully embedded.

In the meantime, the due date(s) for making tax payments will remain the same as they are currently i.e. 31 January following the end of the tax year (and 31 July following the end of the tax year if it is necessary for you to make payments on account).

What will happen if I submit my quarterly updates late?

In the short term HMRC has confirmed it will apply a ‘soft touch’ approach to missed deadlines. Longer term, it is understood that a points based system will be introduced where each missed deadline will accumulate a point and accumulated points will eventually lead to financial penalties. Further details about the new points / penalties scheme are currently unavailable.

Is it only individual taxpayers who will be affected?

Yes.

Making Tax Digital for income tax only applies to ‘individuals’. The new rules to not currently apply to:

- Trusts

- Estates

- Trustees of registered pension schemes

- Formal business partnerships

- UK resident companies

- Non UK resident companies

What will I need to do in between now and 6 April 2026?

In the short term, you may not need to do anything.

However, the key element of Making Tax Digital for income tax is the requirement for taxpayers to maintain business records ‘digitally’. This effectively means using some form of electronic record-keeping system such as an accounting software package, a spreadsheet based system, or an app on a smart device.

HMRC has confirmed it will not produce its own software package to enable digital records to be maintained, so it will be necessary for taxpayers to choose (or indeed purchase) a digital record keeping system that is suitable for their purposes and within their budget.

If you do not already keep your self-employment or property income records in a digital format, you will need to decide, in due course, when to change to a digital record keeping system bearing in mind when you expect to be in the scope to Making Tax Digital for income tax. As discussed above, this will be dependent upon the combined level of gross income from self-employed and property income sources.

HMRC has provided a list of software packages that are compatible with Making Tax Digital for income tax which can be found here:

https://www.gov.uk/guidance/find-software-thats-compatible-with-making-tax-digital-for-income-tax

Are there any exclusions to Making Tax Digital for income tax?

If your combined turnover from self-employment and property does not exceed £20,000 then you will not fall under the scope of the new rules.

It may be possible to apply to HMRC for an exemption from Making Tax Digital for income tax if you are ‘digitally excluded’. This may apply, for example, if you live in a remote location without access to reliable broadband or if, perhaps due to age or disability, it is not reasonably practical for you to use electronic communications or keep digital records.

Exemption may also be available if your religious beliefs are incompatible with using electronic communications or keeping digital records.

Handelsbanken Wealth & Asset Management

Handelsbanken Wealth & Asset Management provides tax compliance and tax advisory services to customers who hold discretionary funds under management in one or more of our investment strategies. If, as a new or existing wealth management customer, you would like to explore how our tax services may benefit you, please ask in branch to speak with one of our Client Directors.

Making Tax Digital for Income Tax

Learning Zone Making Tax DigitalImportant Information

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. This document has been prepared by Handelsbanken Wealth & Asset Management Limited for clients/potential clients who may have an interest in its tax services. These tax services are not regulated by the FCA. The provision of this information does not constitute tax advice.

Although every effort has been made to ensure accuracy, the information provided is based upon our understanding of current tax law and the prevailing practice of HM Revenue & Customs; tax rates and legislation are subject to change. We cannot guarantee to inform you of any such changes and we accept no responsibility for any inaccuracies or errors. Your personal circumstances may affect the outcome of any measures you choose to implement and we recommend you take independent professional advice. We cannot accept responsibility for the consequence of any action taken or failure to take action by a reader on the basis of the information provided. Tax figures and legislation are correct as at April 2024 but are subject to change.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340