8

We’ve all been there – in the queue that’s moving forward at snail’s pace while the one next to you moves along smartly. Losing patience, you switch, only to find that your new queue has ground to a halt as your former queue speeds up! This is a great analogy for investing...

When the market is volatile and prices are falling, it’s tempting to jump to a more promising investment – ‘the grass is always greener’ scenario kicks in. But performance chasing can be a costly mistake – not only due to the narrow investment choices it encourages, but also due to the higher costs and taxes incurred. Overall, investors can end up selling low, buying high and, importantly, missing out on creating long-term value.

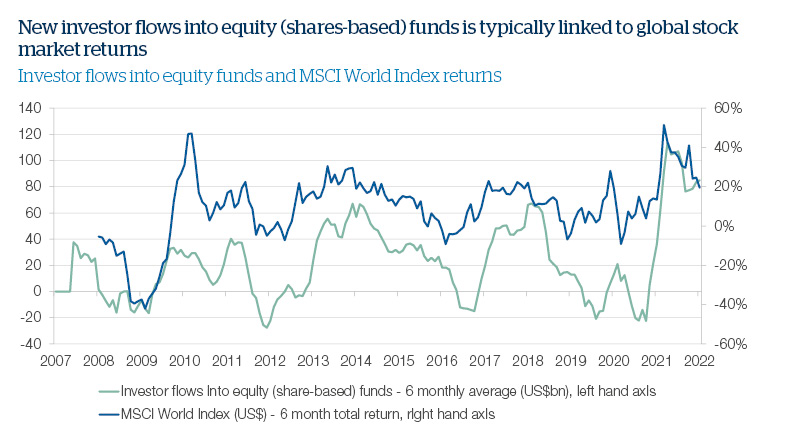

This is demonstrated in the following chart, which shows net new cash flow into equity funds (which invest primarily in shares) from 2008 to 2022. Take a look at the period around the global financial crisis in 2008: investors reacted to market falls by pulling out of shares-based funds in 2009 (green line), but it would have been better to stay put, as the market performed strongly from that point (blue line). A similar reaction occurred after the ‘dot-com bubble’ burst in 2002; the market panic (begun in technology stocks) led to a mass exit from shares-based funds just as markets began an upward surge in 2003. As the chart shows, any investors who behaved in this way during 2020’s market falls were much too hasty: what followed was one of history’s most impressive market recoveries.

Source: Morningstar, MSCI. Past performance is not a reliable indicator of future results.

Taken together, what this indicates is that most investors are not strictly rational and can be subject to behavioural biases, such as past experiences, personal beliefs and preferences, which can influence judgment and skew decisions. These biases can steer them away from logical, long-term thinking, and deter them from reaching their long-term investment goals. It is therefore important to be aware of these biases and their effects. Let’s look at three examples.

1. Reacting to noise

Investors can get caught up in media noise and short-term geopolitical and macroeconomic events. A litany of stories (often negative) from round-the-clock news channels, the internet and social media tends to exacerbate investors’ emotions. They can then put too much emphasis on these short-term events and extrapolate them into long-term themes.

2. Overconfidence

Overconfident investors may overestimate their ability to identify winning investments, whilst at the same time blaming failures on ‘bad luck’ or unexpected events. Chasing winners and selling losers can result in a high degree of short-term trading and potentially a loss-making spiral.

3. Following the herd

People often exhibit herding behaviour or a ‘group think’ mentality when investing. They mimic the behaviour of others, especially in times of uncertainty. However, the majority is not always right, and basing one’s investment decisions on the actions of others makes little sense given everyone’s different investment goals and financial circumstances.

Buy-and-hold requires patience and discipline

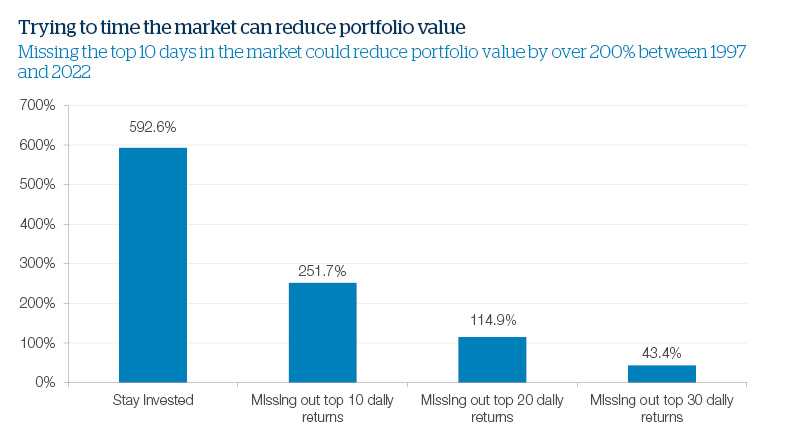

Unfortunately, investors who give into (or are unable to control) their behavioural biases will generally find their investments lag those of investors who adopt a long-term ‘buy-and-hold’ strategy. This is despite the fact that most investors are naturally averse to taking losses. Research shows that losses hurt about 2-2.5 times more than gains satisfy.

A buy-and-hold strategy, though, is not easy; it requires patience and discipline. There may be prolonged periods when the strategy does not appear to be working, but it will ultimately emerge stronger as investments capture the upside throughout market cycles. Having a long-term horizon can therefore help investors to avoid making poor short-term investment decisions. Time in the market - not timing the market - is what’s important.

Source: Macrobond. Past performance is not a reliable indicator of future results.

How to keep focused on long-term goals

Successful long-term investors create diversified portfolios that are tailored to their goals, risk tolerance and time horizon. This is where skilled active managers can help. Active funds will aim to achieve a specific objective by investing in certain assets, with an approach to risk and return that could resonate with an investor’s goals. Using a skilled active manager can add value in both rising and falling markets and can calm investor nerves when markets turn turbulent.

Making money from investments whatever the conditions can be a tall order. However, by using a range of investment tools – including alternative asset types, such as hedge funds, commodities and private equity – to profit from market downs, as well as ups, managers can look to target steady positive returns while limiting potential losses when markets are falling. Positive returns can never be guaranteed, and should not be relied upon, but using this mix of different types of assets can help funds to perform well under different circumstances.

Important Information

Handelsbanken Wealth is a trading name of Handelsbanken Wealth & Asset Management Limited and is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business with firm reference number 197340, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

- Find out more about our services by contacting us on 01892 701803 or exploring the rest of our website: wealthandasset.handelsbanken.co.uk

- Read about how our investment services are regulated, and other important information: wealthandasset.handelsbanken.co.uk/important-information

- Learn more about wealth and investment concepts in our Learning Zone: wealthandasset.handelsbanken.co.uk/learning-zone/

- Understand more about the language and terminology used in the financial services industry and our own publications through our Glossary of Terms: wealthandasset.handelsbanken.co.uk/glossary-of-terms/

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340