8

What is an ISA?

An ISA is an Individual Savings Account which allows you to reap the benefits of your savings and investments free of tax. All ISAs allow you to save and invest without paying UK income or capital gains tax, therefore if you have a sizeable savings pot, ISAs could potentially save you quite a lot in tax.

How much can I save in an ISA?

Each tax year (6 April to 5 April), you get an ISA allowance which sets the maximum you can save within an ISA account. You have until one minute to midnight on 5 April each year to add money to your ISA, as you are not allowed to carry over the allowance to the next tax year.

In the 2025/26 tax year the allowance is £20,000 per year.

You can divide your allowance between different types of ISAs, but the total you save must not be more than £20,000.

The ISA allowance is only for the money that you put into ISAs each year. It doesn’t include the total amount that’s in your ISA from previous tax years, or the money you earn from investments in your ISA.

Any savings or investments which stay within the tax-free ISA wrapper will continue to earn interest (or see investment growth/loss) and reap the tax benefits until you withdraw the money.

Are there different types of ISA?

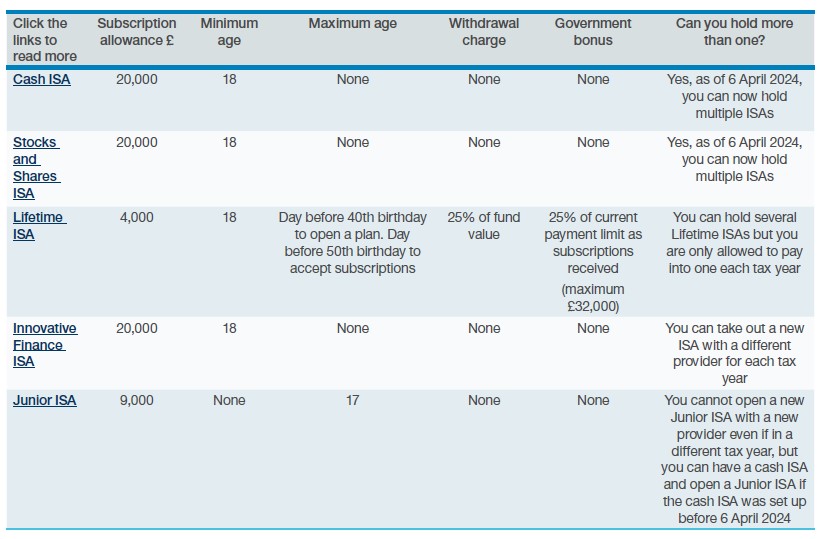

There are five different types of ISA:

- Cash

- Stocks and Shares

- Lifetime

- Innovative Finance

- Junior

You can choose whether you want to invest the whole allowance in to one type of ISA, or whether you want to split it between different types. However, even if you choose to split it, you can't invest more than a total of £20,000 across the different types. And if you have a Lifetime ISA you can only invest a maximum of £4,000 in any one tax year, leaving you a £16,000 allowance for other ISA types.

Cash ISAs

Similar to a regular savings account, but you don’t pay tax on any interest earned. Cash ISAs may be: easy-access where you can access your cash whenever you need without penalty; notice Cash ISAs where you need to give a certain number of days' notice to withdraw your cash, or fixed rate Cash ISAs which tend to offer higher rates than easy-access or notice ISAs, though usually carry an interest penalty if you access your cash before the fixed term expires.

Stocks and Shares ISAs

These allow you to invest your money in funds (shares or bonds from various companies pooled into one investment), and other types of investments, such as bonds (basically a loan to a company or a government), and shares in individual companies.

One of the main benefits of a Stocks and Shares ISA is that you don’t pay tax on any gains from your investments. But there are usually some fees you need to pay with this type of ISA.

It is also important to remember that investing involves various levels of risk and the value of your investments can go down as well as up depending on how well your funds, bonds and shares perform. Taking a long-term approach to investing means allowing your investment to access better growth over time. Investing is different from saving because it involves a greater level of risk. There is no guarantee that you’ll get your money back. You can find out more about the difference between saving and investing by watching our Bite-sized explainer: Saving & investing.

Lifetime ISAs

Lifetime ISAs were launched in 2017 to help people save for their first home, or for retirement.

The government pays in an extra £1 for every £4 you save. You can save up to £4,000 a year into a Lifetime ISA, which becomes £5,000 when the government’s contribution is included. To open a Lifetime ISA, you must be under 40, but you can make contributions up to your 50th birthday.

You can open a Cash Lifetime ISA or a Stock and Shares Lifetime ISA. You may have both types, although you can only open one Lifetime ISA in each tax year, and you can only pay into one each tax year.

You can only withdraw cash from Lifetime ISAs if you're buying your first home or you're 60 or over. You will face a penalty of 25% if you withdraw at any other time (effectively removing the government’s contribution).

If you've saved the maximum £4,000 in a Lifetime ISA in any tax year and you've spare cash left over to save, you can also hold one or more of the other types of ISA in this guide – though remember that your allowance for those will be a maximum of £16,000 in the same tax year.

Innovative Finance ISAs

An Innovative Finance ISA allows you to use the ISA allowance to lend funds directly to other investors.

How this works is the company offering the ISA uses your money to lend to borrowers or businesses (this is often known as peer-to-peer lending). You receive a proportion of the interest rate charged to the borrower for their loan.

While interest rates tend to be generous with Innovative Finance ISAs, as with any form of investing, your capital is at risk and you could lose money, if the people you've lent to can't repay. Risks are somewhat reduced by spreading your cash across multiple loans, or with provider-backed safeguard funds, but if a lot of the borrowers defaulted, it's likely your savings could take a significant hit. It can also take a while to get your money back if you want to withdraw your cash from an Innovative Finance ISA.

Junior ISA (JISA)

This is a long-term savings account set up by a parent or guardian, specifically for their child. Only the child can access the money, and only once they turn 18. The child can have a cash JISA and a stocks and shares JISA, but only one of each type.

Up to £9,000 a year can be saved in a JISA. This is less than a half of the adult ISA allowance, but it is a separate allowance – so you could save £20,000 in your ISA, and £9,000 into your child's JISA in the same tax year.

You can divide the annual JISA allowance between a cash JISA and a stocks and shares JISA. The account is held in the child's name but is opened and managed by the parent or guardian. The child can take control of the ISA at 16, but cannot withdraw the cash until 18.

Prior to the Budget announcement in March 2024, an unusual quirk of the system meant that a child of 16 or 17, could have two ISA allowances – the JISA allowance of £9,000 plus the adult cash ISA allowance of £20,000. However, the 2024 Budget altered this dynamic by aligning cash ISAs with other ISAs, requiring individuals to be now be 18 to open a cash ISA. However, you can still contribute to a cash ISA if you are 16 or 17 providing that this was set up before 6 April 2024.

Can I have more than one ISA?

Yes, there is no defined upper limit on how many you can have in total.

Until 6 April 2024 you could only open one of each type of adult ISA per tax year. However this has changed and you are now able to pay into multiple ISAs of the same type each year as long as you don't exceed your ISA allowance.

Can I replace the money I have taken out of my ISA?

Except for the Lifetime ISA, you can take your money out of an ISA at any time, without penalty. If your ISA is described as ‘flexible’ by your ISA provider, then you can take out cash and put it back in during the same tax year without reducing your current year’s allowance.

Can I transfer my ISA to a different provider?

You can switch between providers of the same ISA type, but do be aware that there may be fees and interest penalties to pay to your current provider.

The most important thing to remember is to never withdraw all your money yourself to make the transfer. Your savings could lose their tax-free status as a result.

Your new provider will provide you with a transfer form to complete and will manage the process for you, including contacting your current provider, and moving the money over for you.

You can also transfer over previous year's ISA savings too – this is especially useful if you've several different ISAs from previous tax years and you want to consolidate them into one account.

An update following the October 2024 Budget:

The annual subscription limits for Individual Savings Accounts (ISAs) Junior Individual Savings Accounts (JISAs), Lifetime Individual Savings Accounts (LISAs), and Child Trust funds will remain unchanged until April 2030.

Although announced in 2024's Spring Budget, proposals for the new 'British ISA' have now been scrapped.

Understanding ISAs

Learning Zone Understanding IsasImportant Information

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. This document has been prepared by Handelsbanken Wealth & Asset Management Limited for clients/potential clients who may have an interest in its tax services. These tax services are not regulated by the FCA. The provision of this information does not constitute tax advice.

Although every effort has been made to ensure accuracy, the information provided is based upon our understanding of current tax law and the prevailing practice of HM Revenue & Customs; tax rates and legislation are subject to change. We cannot guarantee to inform you of any such changes and we accept no responsibility for any inaccuracies or errors. Your personal circumstances may affect the outcome of any measures you choose to implement and we recommend you take independent professional advice. We cannot accept responsibility for the consequence of any action taken or failure to take action by a reader on the basis of the information provided. Tax figures and legislation are correct as at April 2024 but are subject to change.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340