Investment Team Handelsbanken Wealth & Asset Management

16 Apr 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Keeping pace with global tariffs is becoming a full-time job

A distinctly unwelcome guest has entered the global economy in the opening weeks of Trump’s second presidency: worldwide trade tariffs. They’ve also proven to be a rather erratic guest, changing with little or no notice, and creating huge swings in both financial markets and economic growth projections in the process.

As we’ve said in previous updates, it’s hard to create an update on the global picture without immediately going out of date. As we write this, a 10% ‘universal’ trade tariff is being applied to goods entering the US, though some countries (like Mexico and Canada) are subject to more complex and variable trading agreements. At the most extreme end of the scale, the average tax on goods going between the US and China now exceeds 140%. Meanwhile, other countries around the world have been given 90 days to negotiate new trading terms with the US.

Are bond markets Trump’s weakness this time around?

The US is the world’s largest economy and the most influential financial market: what happens in the US almost always ultimately impacts the global picture. But by actively influencing other regional economies through trade tariffs, the impact today is more extreme and immediate.

To say the least, financial markets do not like Trump’s tariffs. Stock market performance has swung about wildly, while bond markets have been decidedly unforgiving. The price of US Treasuries (government bonds) has fallen aggressively – a very unusual phenomenon for this famously stable area of bond markets. The US 30-year Treasury recently experienced one of its largest price drops in decades. (As a reminder, bond yields move in the opposite direction to bond prices, and have risen sharply in recent history.)

When Trump was first in office, he appeared to be heavily influenced by stock market performance, perhaps viewing US share prices as a barometer for his success. With his second term in the White House now underway, it looks like bond markets may have taken on this role instead. It’s easy to view Trump’s sudden announcement of a 90-day negotiation window for international tariffs as a response to the turmoil in US Treasuries, and the alarm it has caused to the US establishment.

Fighting the impulse to run and hide

We understand completely that this is an unnerving market environment for our customers. Staying the course when markets are volatile is not easy; it requires patience and discipline, and a focus on the long term. We know that it’s incredibly tempting to become caught up in media noise and short-term events.

No outcomes can ever be guaranteed, but our view is that in times of high turbulence, it’s broadly better to hold one’s nerve and remain invested in global markets. Trying to perfectly time exit and entry points in financial markets is a notoriously fraught undertaking, and can result in serious damage to long-term financial outcomes. If you’d like to learn more about this, we would really recommend taking a look at our Learning Zone article on just this topic.

Most importantly, if you’re feeling nervous about the recent events in financial markets and would like more information, please do get in touch.

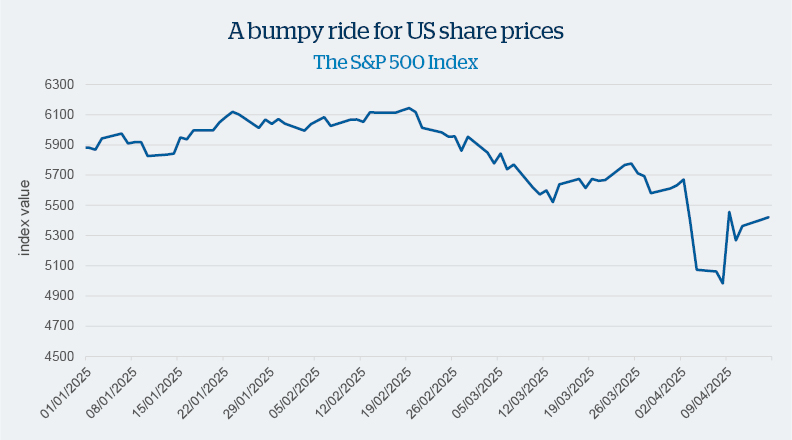

Source: Macrobond

The S&P 500 Index represents the share prices of the 500 largest companies listed on US stock exchanges. Trump’s tariff wars have led to large swings in this index, with share prices shooting higher and lower as investors try to account for the impact of tariffs upon the share prices of US businesses.

Highlighting this stock market volatility, on Wednesday 9 April, the S&P 500 Index saw its largest daily move since the 1950s. It’s worth noting that while falls in share prices can be alarming, in the right situation, they can also present buying opportunities. As ever, no outcomes are ever guaranteed, and risks work in both directions – up and down.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are slightly 'overweight' stock markets/shares. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively larger proportion of investments in stock markets versus our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

The ‘alternative’ investment space covers a diverse range of assets outside of traditional bond and stock markets, from commercial property to specialist hedge funds. Because of their wide variety, it’s difficult to make sweeping statements about alternative assets, and our overall ‘underweight’ stance in this diverse area of the markets hides some specific preferences.

At present, we have a preference for assets which can drive financial returns, without being closely linked to mainstream financial markets. Among our positions in property investments, we have a preference for global assets over UK-based assets, believing that this allows us to access a much more diverse array of property, from data centres to telecoms towers.

Other notable positions include a long-term portfolio position in gold, and a specialist hedge fund designed to protect against dramatic market falls.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340