Investment Team Handelsbanken Wealth & Asset Management

19 Aug 2025 15

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Below, we outline some of our key views on the factors set to drive financial markets over the coming months, and what this means for our investment strategies.

Tariff wars are still providing surprises

As August began, the US imposed trade taxes on most countries which had not managed to negotiate a trade deal with President Trump. The highest tariff was given to Brazil (50%), while China’s deadline has been pushed back into the Autumn. For Trump, tariffs are also a lever to pull as he attempts to control and contain other global issues. For example, the US president has threatened to hike tariffs to 50% on imports from India to the US, unless India stops buying Russian oil. Financial markets were exasperated by the drama of the tariff deadline day, and stock markets initially dipped (albeit staging a recovery just a few days later).

Is there trouble at home for President Trump?

But while tariffs continue to dominate the headlines, investors are growing worried about the domestic picture in the US. There are signs of weakening economic data in critical areas, including faltering employment markets and worse-than-expected private sector business survey data. Meanwhile, Trump has also made a show of threatening the relative independence of various important public bodies. This has included firing the Commissioner of the Bureau of Labor Statistics (not strictly an independent body, but usually insulated from direct political control) as well as pressurising the US central bank to cut interest rates, and openly disapproving of their decision not to do so in August. All eyes will be on the central bank’s next meeting in September, when markets do see potential for a rate cut.

The Bank of England is a house divided

At its August meeting for leading policymakers, the Bank of England reduced its benchmark interest rate to 4%, as widely expected. However, the Bank’s leaders were unusually polarised, requiring an historic second vote in order to reach a majority decision. The Bank has a ‘dual mandate’, meaning that it must manage the dynamics of both inflation and economic/employment stability. This is proving challenging, especially since the Bank has also raised its forecast for UK inflation. Following this latest update, investors have toned down their expectations for further UK interest rate cuts in the near term.

How are our investment strategies positioned for the next chapter?

We’ve spent the past 18 months or so simplifying our investment positions and making them exceptionally ‘liquid’ – ready to move easily if need be. Our investment strategies are well-diversified across different types of financial assets, including our stock market positioning, where we’ve previously slightly reduced our exposure to the choppy US market.

As we’re sure our clients already know, investing always means exposing your capital to the possibility of both rises and falls in financial markets, presenting both risks and opportunities. It’s our privilege to help you understand more about this, so if you would like more information, please do get in touch.

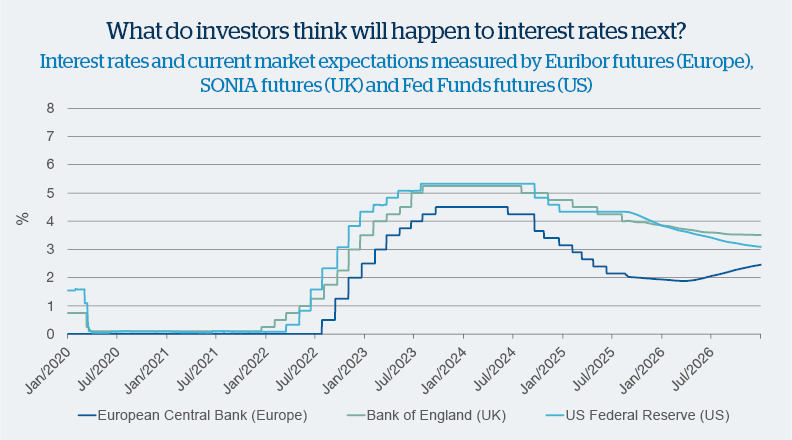

Source: Macrobond

The chart shows historical interest rates with current market expectations by central banks in the US, UK and Europe. The Bank of England and European Central Bank have been making interest rate cuts relatively steadily, but the US Federal Reserve (Fed) has been hanging back of late, and it looks like markets expect the Fed to continue to play the laggard for a little while longer.

Like the Bank of England, the Fed has more than one goal: it must manage price stability (inflation) as well as creating the conditions for high and sustainable employment levels. At the moment, the Fed is being pulled in two directions at once: cracks are appearing in employment markets, which would suggest that the Fed should cut rates to support economic growth (which would enable job creation), but inflation is also high (in part thanks to tariff expenses), which would normally mean making interest rate hikes to take some of the heat out of the economy. For now, the Fed appears to be in ‘wait and see’ mode, keeping an eye on economic data and political/international events before it commits to its next step.

Scroll down the page to the sections below to find out what our market views mean for positioning in our investment strategies.

At the time of this update, we are 'neutral' stock markets/shares. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in stock markets which is consistent with our long-term average.

At the time of this update, we are 'neutral' when it comes to bond markets. This means that we have not deviated for tactical reasons from our overall asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a proportion of investments in bond markets which is consistent with our long-term average.

At the time of this update, we are slightly 'underweight' alternative assets. This means that we have deviated for tactical reasons from our asset allocation framework - a way of dividing investments across different types of assets. As a result, our multi asset strategies currently hold a relatively smaller proportion of investments in alternative assets versus our long-term average.

If you’d like further information on how we divide investments in our strategies across different types of assets (i.e. our asset allocation framework, and our tactical deviations away from it), please contact us.

Handelsbanken Wealth & Asset Management Limited is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

This document has been issued by Handelsbanken Wealth & Asset Management Limited. For Handelsbanken Multi Asset Funds, the Authorised Corporate Director is Handelsbanken ACD Limited, which is a wholly-owned subsidiary of Handelsbanken Wealth & Asset Management, and is authorised and regulated by the Financial Conduct Authority (FCA). The Registrar and Depositary is The Bank of New York Mellon (International) Limited, which is authorised by the Prudential Regulation Authority and regulated by the FCA. The Investment Manager is Handelsbanken Wealth & Asset Management Limited, which is authorised and regulated by

the FCA.

Before investing in a Handelsbanken Multi Asset Fund you should read the Key Investor Information Document (KIID) as it contains important information regarding the fund including charges and specific risk warnings. The Prospectus, Key Investor Information Document, current prices and latest report and accounts are available from the following webpage: wealthandasset.handelsbanken.co.uk/fund-information/fund-information/, or you can request these from Handelsbanken Wealth & Asset Management Limited or Handelsbanken ACD Limited: 77 Mount Ephraim, Tunbridge Wells, Kent, TN4 8BS or by telephone on

+44 01892 701803.

Registered Head Office: No.1 Kingsway, London WC2B 6AN. Registered in England No: 4132340