Investment Team Handelsbanken Wealth & Asset Management

10

This website and all the information provided on it is intended for users domiciled in the UK only. By continuing you are confirming that you have read the important information and understood the legal information contained within. You are also consenting to the use of cookies on this site.

Bonds are one of the world's oldest financial instruments. They are a form of debt, and are effectively IOUs between counterparties.

Bond are also known as ‘fixed income’ assets, reflecting the interest they pay out to their holders, which provides an income stream.

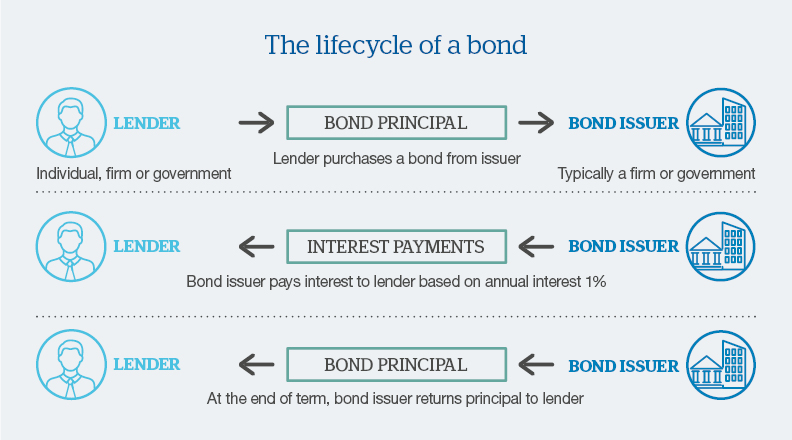

Bonds have their own terminology, which some non-specialist investors may find off-putting. Yet at their heart, bonds can be viewed as relatively simple assets. The chart below illustrates the lifecycle of a simple bond.

On one side are the bond issuers, who need the loan/credit. On the other are the lenders who expect their loan (the ‘principal’) to be repaid at an agreed future date. To make the transaction commercially attractive for lenders, the bond issuer will also pay out interest (the ‘coupon’) to the lender at regular points during the lifetime of the loan (until its ‘maturity’).

When bonds are sold directly to end buyers, this is known as primary issuance. Bonds that have already been issued can trade on secondary market, in a similar way to company shares.

A key moment in the development of credit markets and capitalism was the Protestant Reformation at the beginning of 16th century. Before then, usury (the charging of interest on a loan) went against the Church’s teachings.

The first central bank to issue bonds was the Bank of England, in 1694, while the Dutch East India Company (as with company shares) was one of the first companies to issue bonds.

Up to the 1970s, bonds were used primarily by central banks, organisations like the World Bank and large companies. They are now issued by a wider range of institutions and supply investors with a much broader range of investment characteristics.

Bonds are a very important part of modern global financial markets. Global bonds accounted for $130bn in assets at the end of 2022, compared to the $101bn value of world stock.

Owning a bond can be likened to owning a collection of future cash payments. First, a stream of regular interest payments, then later ending with the repayment of the principal (the original amount you lent out) when the bond ‘matures’.

Traditional bonds payments will be through fixed or floating (interest) rates.

One of the most important features of a bond is the inverse relationship between its price and its yield. The interest paid on the bond remains fixed (though it may be fixed to move in line with factors like inflation, for some bonds), but the price of the bond in secondary markets can fluctuate. When bond prices rise, their overall yields fall. When bond prices fall, their yields rise.

A fixed rate bond provides a bond holder with same level of regular interest payment throughout the lifetime of the bond.

The interest payments on a floating rate bond fluctuate throughout the lifetime of the bond. They could be tied to the central bank’s interest rates, for example.

In addition to fixed and floating interest rate bonds, other types of bonds include:

These bonds do not pay interest to their holders. They are sold at a discount to their face value, meaning that the principal returned at maturity is larger than the initial amount paid for the bond.

Very unusual bonds whose interest payments have no end date. While the principal invested is never returned, in theory the interest payments go on forever.

The interest payments on these bonds are linked to inflation (which could rise or fall). These bonds are aimed at minimising the impact of inflation for their holders.

These bonds offer the right to convert the bond into a predefined number of company shares.

One of the most important features of a bond is the inverse relationship between its price and its yield. The interest paid on the bond remains fixed (though it may be fixed to move in line with factors like inflation, for some bonds), but the price of the bond in secondary markets can fluctuate. When bond prices rise, their overall yields fall. When bond prices fall, their yields rise.

Bonds that pay a fixed interest rate become more desirable versus the rates investors can earn on cash. This drives their prices higher.

Bonds that pay out a fixed interest rate will be less attractive versus the interest rates which can be earned on cash. This drives their prices lower.

No asset is risk free but bonds are generally considered a less risky asset compared to company shares.

Cautious investors may benefit from the income stream that bonds provide as well as the repayment of the principal on maturity. In contrast, investors with a higher risk profile will often seek out bonds that can provide higher returns, such as bonds issued by companies or developing market governments. Like shares, these types of bonds will typically expose investors to a higher level of risk.

Perhaps the greatest danger from investing in bonds is default risk, i.e. the inability of the bond issuer to pay interest payments or repay the principal to the bondholders. This is why all bonds are provided with a bond rating from a ratings agency, such as Moody’s, Fitch Ratings or Standard & Poor’s. These ratings assess a bond’s financial strength and its ability to repay bondholders. The highest quality bonds (‘investment grade’) are deemed to have the lower risk, and consequently should deliver the lowest returns.

While the basic principles of bond investing can seem very simple, some of the associated language can seem confusing. Below are some frequently used terms:

The market for corporate bonds – bonds issued by businesses rather than governments.

This measures the sensitivity of a bond’s price to changes in interest rates. A bond with ‘high duration’ is more sensitive to changes in interest rates than one with ‘low duration’.

Issued and backed by governments, these are considered low risk investments, backed by a government’s credit. Broadly speaking, bonds issued by countries in developed countries like the UK and US are considered safer than those issued by governments in developing economies like China and India.

These are higher yielding bonds, issued by companies with lower credit ratings. They offer higher interest rates to compensate for the higher risk taken on by the bond holders.

The degree of fluctuation in the price of a bond. A bond with higher volatility is prone to excessive price fluctuations.

The rate of return an investor receives if the bond is held to maturity.

Traditionally, bond and equity prices have an inverse relationship – that is, when share prices rise, bond prices will often drop as investors switch into the higher potential returns offered by shares. Likewise, bond prices tend to benefit when share prices fall. Conventional investing wisdom emphasises the benefits of diversification, often expressed as an investment portfolio split 60-40 between equities and bonds.

There are two ways in which we purchase bonds for our investment funds:

We may buy bonds directly in the open market.

By purchasing bonds through collective instruments, either using exchange traded funds (ETFs), which are baskets of securities trading a market index, or those operated by another investment manager. This latter method will only be used if it is the best way of achieving our investment goals.

Yes, and in fact we would recommend this approach for the most investors.

Diversification should be an important consideration when building an investment portfolio for the long term.

One way to achieve this is by a mix of different assets including shares, bonds and alternative assets. Their performance will likely be uncorrelated and can help to generate the desired level of financial returns. Taking a blended approach in this way is often called ‘multi asset investing’.

If you’d like to find out more about multi asset investing, please explore our Learning Zone, where we have more resources on this topic.

Handelsbanken Wealth is a trading name of Handelsbanken Wealth & Asset Management Limited and is authorised and regulated by the Financial Conduct Authority (FCA) in the conduct of investment and protection business with firm reference number 197340, and is a wholly-owned subsidiary of Handelsbanken plc. For further information on our investment services go to wealthandasset.handelsbanken.co.uk/important-information. Tax advice which does not contain any investment element is not regulated by the FCA. Professional advice should be taken before any course of action is pursued.

All commentary and data is valid, to the best of our knowledge, at the time of publication. This document is not intended to be a definitive analysis of financial or other markets and does not constitute any recommendation to buy, sell or otherwise trade in any of the investments mentioned. The value of any investment and income from it is not guaranteed and can fall as well as rise, so your capital is at risk.

We manage our investment strategies in accordance with pre-defined risk objectives, which vary depending on the strategy’s risk profile.

Portfolios may include individual investments in structured products, foreign currencies and funds (including funds not regulated by the FCA) which may individually have a relatively high risk profile. The portfolios may specifically include hedge funds, property funds, private equity funds and other funds which may have limited liquidity. Changes in exchange rates between currencies can cause investments of income to go down or up.

Registered Head Office: 25 Basinghall Street, London EC2V 5HA. Registered in England No: 4132340